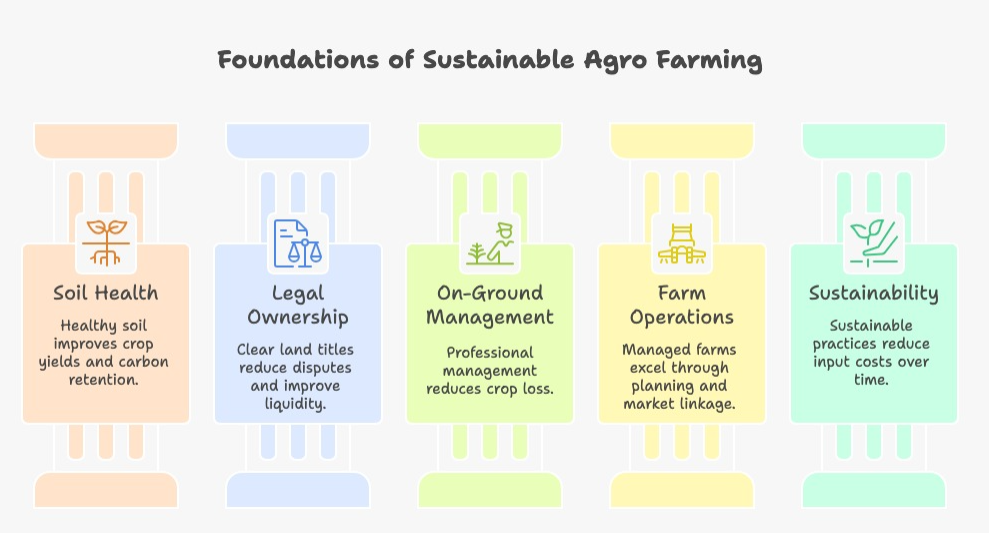

For most of my life, I have worked with land—not as a product, not as a commodity, but as a living system.

Over time, one pattern became impossible to ignore.

People who rushed land lost patience. People who respected land gained resilience.

Today, as capital becomes volatile and attention spans shorten, something interesting is happening quietly across India. Thoughtful individuals are stepping away from fast money and returning to agro farming land investment—not as nostalgia, but as strategy.

2. Is agro farming land investment legal in India?

Yes, agro farming land investment is legal in India, provided it complies with state-specific agricultural land laws, land-use classifications, and ownership eligibility norms. Proper title verification, registration, and mutation are essential before any purchase.

3. Can non-agriculturists invest in agro farming land investment?

4. Are returns guaranteed in agro farming land investment?

No. Agro farming land investment does not offer guaranteed or fixed returns. Agricultural outcomes depend on climate, soil health, crop cycles, and market conditions. Responsible models focus on transparency, risk disclosure, and long-term value rather than short-term promises.

5. How does agro farming land investment generate income?

Income in agro farming land investment is generated through actual agricultural activity such as orchard produce, intercropping, allied activities like honey or dairy, and sometimes agri-tourism. Land appreciation over time also contributes to overall value.

6. How important is soil quality in agro farming land investment?

7. What crops are commonly chosen for agro farming land investment?

Crop selection depends on agro-climatic conditions. In suitable regions, long-term orchard crops such as mango, cashew, coconut, and mixed horticulture are preferred because they support sustainable yields and land appreciation.

8. Is agro farming land investment suitable for passive investors?

Yes, agro farming land investment is well suited for individuals who want land ownership without daily farm involvement. Professional management systems handle operations, while owners receive periodic updates and retain full ownership rights.

9. What are the main risks in agro farming land investment?

Risks include weather variability, pest pressure, yield fluctuations, and market price changes. Well-structured agro farming land investment models mitigate these risks through crop diversification, soil regeneration, water management, and transparent reporting.

10. Why is agro farming land investment considered a long-term asset?

Agro farming land investment operates on natural time cycles. Orchards and regenerative farms mature over several years, creating stable productivity and appreciation. This makes it a patient, legacy-oriented asset rather than a speculative one.

I have seen land neglected—and I have seen land transformed.

The difference was never money. It was intention and management.

Agro farming land investment is not a trend. It is a return to intelligence.

When land is owned responsibly, managed professionally, and respected deeply— it becomes a lifelong ally.

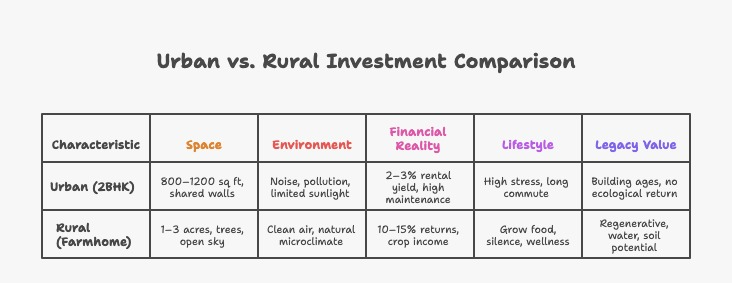

When the Price of a 2BHK Equals the Price of an Entire Ecosystem (Farmland Is the New Asset in India)

There is a moment I often return to — a single conversation that somehow explains India’s entire shift in wealth psychology.

It was a hot afternoon in North Goa. A couple from Delhi visited one of our land ecosystems. They were bright, hard-working, successful — the kind of people who had done everything “right”: saved money, invested in SIPs, worked long hours, and finally reached the familiar milestone:

Later, as we walked across a 2-acre farmland parcel with mature trees, freshwater channels, and a half-done farmhome structure, they asked — almost casually:

“How much does this cost?”

When I told them it would cost about the same as their 2BHK, everything in their body language shifted.

They stood in silence. They listened to the wind. They looked at each other.

And then they asked the question so many Indians are secretly starting to ask:

“Are we crazy to buy an apartment when we can buy a whole world for the same price?”

That day, I realised something India has not yet said aloud:

We have reached the moment where a farmhome can cost the same as an apartment — and often offers 10 times the life.

This is not a privilege anymore. This is not a fantasy. This is not off-grid escapism.

This is a market reality, and it is one powerful reason why farmland is the new asset in India.

In this essay, I want to dissect this shift through every lens — economic, cultural, ecological, psychological, and philosophical — the way I have observed it for over two decades of working with land.

Why the Apartment Dream Is Collapsing Under Its Own Weight

When India saw migrant workers walk home, when shelves ran short of essentials, when cities felt fragile — something deep shifted in our collective subconscious.

We realised:

Food comes from farmers, not apps

Oxygen comes from trees, not cylinders

Peace comes from silence, not screens

And suddenly, owning land wasn’t an old-fashioned idea — it was a future-proof one.

Farmhome: Land appreciation + crop income + ecological value + rental retreat income.

Legacy

Apartment: A structure that ages.

Farmhome: An ecosystem that matures.

This is why more and more families see farmland is the new asset in India as the cornerstone of multi-generational wealth.

My Personal Framework (The KDR Lens)

Whenever I evaluate land, I look through 5 layers:

Soil — Is it alive?

Water — Is it sustainable?

Access — Is it reachable?

Ecology — Is it abundant?

Community — Is it aligned?

Land is not a commodity for me. Land is a relationship.

The Real Question: Which Life Are You Buying?

A 2BHK buys you:

A container

A commute

A routine

A dependency

A depreciating structure

A farmhome buys you:

A horizon

Trees

Oxygen

Freedom

Soil

Food

Water

Legacy

Identity

One asset shelters you. The other transforms you.

FAQs

1. Why are more Indians choosing a farmhome over an apartment?

Many Indians are realising that an apartment is a depreciating structure, while farmland is a living, appreciating ecosystem. A farmhome gives you land, water, trees, silence, food production, and space — often for the same price as a 2BHK in a metro.

Apartments offer convenience, but farmland offers continuity. With rising urban stress, food inflation (RBI data), and climate-related anxiety, people are choosing land because it gives emotional stability along with financial returns. That’s why farmland is the new asset in India — it delivers multi-dimensional value beyond square feet.

2. Is farmland actually a good investment compared to an apartment?

Yes — especially over a 10–20 year horizon. According to Times of India, farmland in many regions has appreciated 12–20% annually, while managed farmland models (Mint, ET Wealth) yield 10–15% returns.

Apartments, on the other hand, often plateau after the initial sales cycle, and buildings deteriorate over time. Farmland appreciates with ecological restoration, water security, and improved rural infrastructure — and it can produce income through crops, leasing, or nature-based tourism.

3. Can I legally buy farmland in India if I’m not a farmer?

Yes, in many states — with certain conditions. States like Karnataka, Telangana, Tamil Nadu, and Rajasthan have relaxed old restrictions (ET Realty). However, rules vary widely.

A well-managed farmhome can earn both active (crops, rentals) and passive income (carbon credits, agroforestry yield).

7. Is farmland safer from inflation compared to urban property?

Absolutely. Food inflation directly increases the value of agricultural land. RBI data shows India’s food inflation consistently high over the last several years.

Urban apartments, meanwhile, do not benefit from inflation — their maintenance costs rise while rental yields remain stagnant.

Farmland holds intrinsic value because it produces calories, not just currency. That is why farmland is the new asset in India during inflation cycles.

8. What determines the value of farmland long-term?

Five layers determine farmland value — my KDR Framework:

Soil quality

Water security

Access and infrastructure

Ecological resilience

Community and local culture

If these five align, farmland becomes a generational asset. If even one collapses, the value collapses with it.

9. Can a farmhome replace a primary residence?

Yes — for some families. More Indians (especially hybrid workers) are shifting to primary living on farmland and keeping small city apartments for convenience.

With lifestyle migration, air quality concerns, and rising real estate prices, many people see a farmhome as a healthier, more sustainable place to raise children.

10. Are apartments still better for rental income than farmland?

Apartments can offer rental income, but yields are often 2–3% per year, barely covering maintenance.

A thoughtfully designed farmhome or farmstay can outperform this through:

Eco-tourism

Weekend rentals

Retreat hosting

Wellness experiences

Plus, farmland yields appreciation + ecological value — things an apartment cannot match.

Climate change increases urban heat, raises food prices, strains supply chains, and makes water resources scarcer (World Bank).

Farmland with:

water

trees

regenerative capacity

…becomes a climate haven.

As extreme weather intensifies, people are seeking nature-based living systems — positioning farmland as the new asset in India for climate-adapted wealth planning.

12. Should first-time investors consider farmland instead of a second apartment?

For many, yes. A second apartment often brings:

High EMI

Low yield

High maintenance

Stressful tenants

A farmhome brings:

Land appreciation

Emotional ROI

Access to nature

Food security

Carbon & ecological potential

Health benefits

A legacy to pass on

If your investment horizon is 10+ years, and if you desire a meaningful asset rather than a speculative one — farmland may offer far more value than a second flat.

The Future of Indian Wealth Is Returning to Its Oldest Form

After 25 years of building land ecosystems, I can say this with conviction:

Wealth does not lie in walls. Wealth lies in the soil.

When markets panic, the land remains calm. When inflation rises, the land becomes valuable. When cities choke, the land breathes. When the world changes, the land remains.

This is why farmland is the new asset in India — not because it is fashionable, but because it is true.

A farmhome at the price of an apartment is not a choice between two properties. It is a choice between two lifestyles, two philosophies, two futures.

And if you choose the soil — I believe you are choosing a life your children will thank you for.

Delhi Pollution Analysis 2025: The Winter That Warned Us About the Next 10 Years

THE MORNING DELHI COULD NOT BREATHE

On 6 December 2025, Delhi woke up to what looked like another serene winter morning. Soft sunlight, slightly chilled air, a quiet stillness across the city — the kind of morning we romanticise in stories and postcards.

But Delhi’s winter beauty has learned to hide its wounds well.

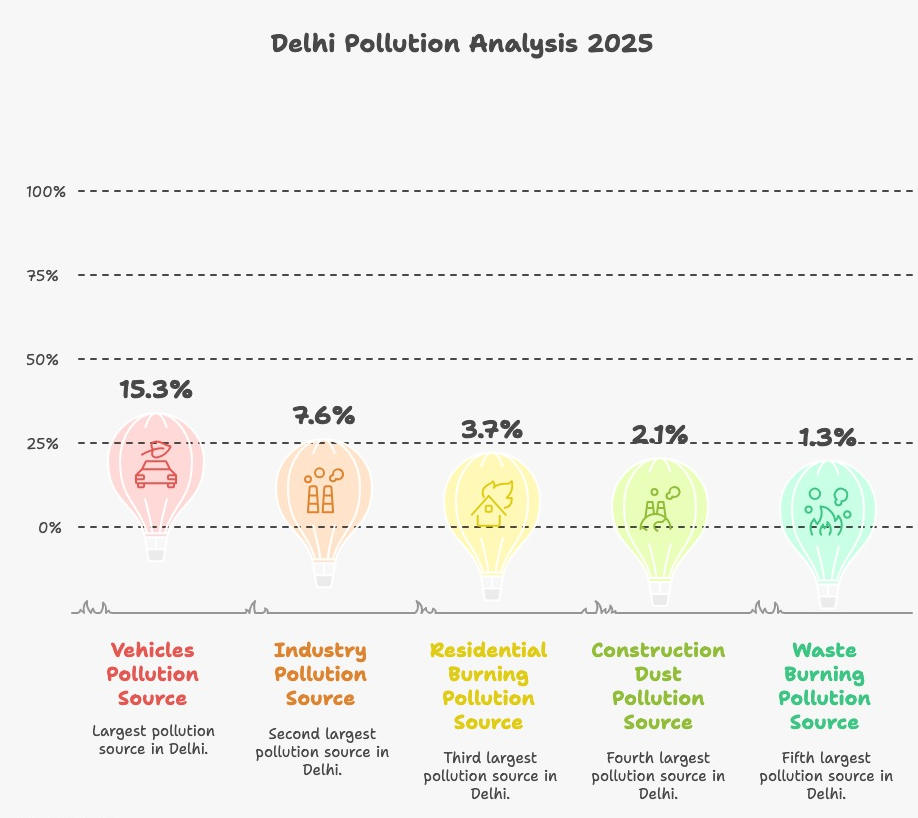

Behind that gentle atmosphere was a truth severe enough to shake any city, any leader, any parent, any human: Delhi recorded a 24-hour average AQI of 333 according to the Central Pollution Control Board.

People drove to work. Children left for school. Construction cranes turned. Joggers ran through what they thought was mist, but was in fact microscopic harm engineered by our own systems.

This is where a real Delhi pollution analysis begins — with honesty, with discomfort, and with a recognition that air pollution is not an air problem at all. It is a land problem, a soil problem, a systems problem, and ultimately, a reflection of how we have built our lives around speed instead of sense.

Let us walk through this story fully — how the crisis began, what is causing it, what the facts truly reveal, and what our next 10 years will look like if we continue this relationship with land and air.

THE DAY DELHI COULD NOT BREATHE — DECEMBER 6, 2025

A meaningful Delhi pollution analysis starts with the numbers because numbers don’t lie, even when people do.

Respiratory diseases become chronic. Medical costs rise. Health inequality widens.

3. Talent migration out of Delhi

People move to cleaner microclimates.

4. Real estate in polluted pockets stagnates

High-value zones lose desirability.

5. Children suffer cognitive decline

Pollution affects brain development. This is backed by multiple WHO studies.

6. Soil continues to die

Air pollutants deposit heavy metals into soil.

7. Psychological toll

Life becomes anxious, restricted, and health-driven rather than joy-driven.

This is the Delhi we drift toward if we simply “manage pollution” instead of transforming systems.

THE CITY WE REIMAGINE

Now imagine the opposite — a Delhi that chooses regeneration over crisis response.

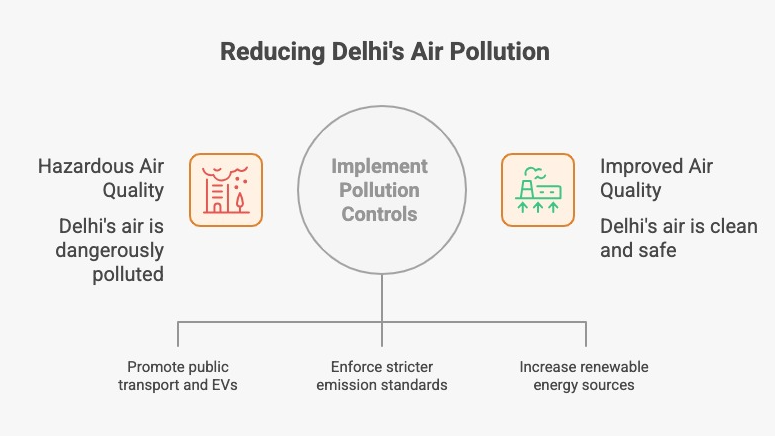

1. A transportation revolution

Electric buses dominate

Last-mile mobility is electric

Private vehicles reduce

Cycling lanes and pedestrian zones expand

2. Land regenerates

Delhi restores:

Wetlands

Ridge forests

Yamuna floodplains

Urban biodiversity corridors

Peri-urban agroforestry zones

Land begins to heal — and so does air.

3. Construction becomes dust-free

AI-based monitoring ensures compliance.

4. Health system integrates AQI

Doctors track patient exposure by pin code.

5. Clean-air geographies become wealth zones

People invest in:

Hills

Coastal belts

Forest-edge communities

Regenerative developments

6. Delhi breathes again

Children play outside. Winter smells like winter, not chemicals. The sky is blue more often than grey.

This is not fantasy. London did it. Beijing did it. Mexico City did it.

Delhi can too.

WHY DELHI’S POLLUTION IS A LAND STORY

My core belief remains:

Air is land in motion.

If the land is:

Sick

Dry

Hard

Eroded

Treeless

Toxic

Then the air will be too.

A real Delhi pollution analysis must address:

Soil health

Floodplains

Water cycles

Green cover

Biodiversity

Heat islands

Ecological systems

Fix the land → fix the air. Ignore the land → the air will reveal our neglect every winter.

FAQs

1. What does the Delhi pollution analysis for 2025 reveal about the city’s air quality?

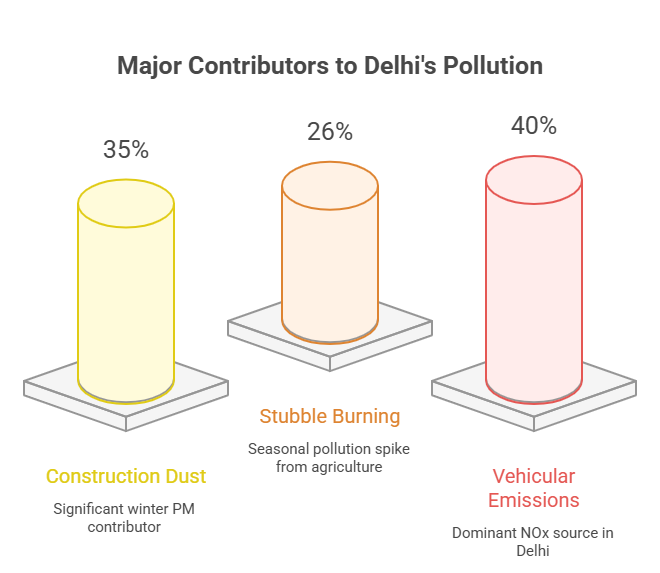

The Delhi pollution analysis for 2025 reveals that pollution is no longer a seasonal inconvenience — it has become a structural feature of the city. December 6, 2025, recorded an AQI of 333, and November saw multiple “Severe” days where AQI crossed 400+. This means Delhi’s air contains toxic levels of PM2.5, NOx, ozone, and black carbon, significantly above WHO safety limits.

The analysis shows that pollution is not an event — it is a symptom of deeper land mismanagement, unregulated construction, vehicular emissions, and the collapse of ecological buffers like rivers, soil, and tree cover.

2. Why is PM2.5 such a major concern in Delhi pollution analysis?

PM2.5 is the most dangerous pollutant because it is small enough to enter the bloodstream. In Delhi’s winter, PM2.5 concentrations often reach levels 20–35 times higher than the WHO recommended limits. This results in:

Chronic respiratory diseases

Cardiovascular stress

Cognitive decline

Impaired lung development in children

Systemic inflammation in adults

PM2.5 doesn’t just irritate — it alters the body’s internal systems. That’s why every credible Delhi pollution analysis places PM2.5 at the center of concern.

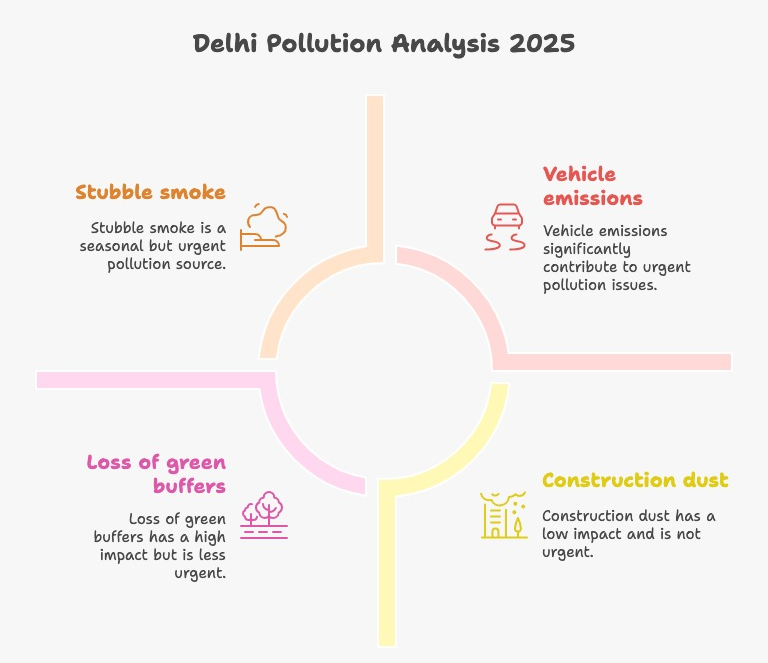

3. What caused the spike in pollution around November–December 2025?

Delhi’s winter pollution spike is a combination of:

Local emissions — vehicles, industry, construction dust, waste burning

Seasonal factors — temperature inversion traps pollutants

Geography — Delhi is landlocked with weak winter winds

Regional influence — stubble burning from neighboring states

Ecological degradation — loss of wetlands, soil moisture, and natural wind corridors

When the city loses its natural defenders — soil, trees, water bodies — the air becomes a storage house for pollutants.

4. How does pollution impact children differently than adults?

Children breathe faster and absorb more pollutants per kilogram of body weight. Pollution impacts them in ways adults may not immediately see:

Reduced lung capacity

Increased asthma and allergies

Lower cognitive performance

Memory and attention issues

Disrupted emotional regulation

Higher lifetime disease risk

In Delhi, a child breathing winter air is undergoing chronic, involuntary exposure therapy, except the substance is toxic.

5. What role does land mismanagement play in Delhi’s pollution?

A deeper Delhi pollution analysis shows this clearly: Air pollution begins with the land.

When wetlands are filled, forests shrink, and soil loses its structure:

Dust increases

Heat islands expand

Moisture decreases

Natural air purification collapses

Pollutants settle into the city instead of dispersing

The land is Delhi’s first air filter. When the land stops breathing, the city stops breathing too.

6. How does pollution affect the long-term economic and real estate landscape?

Air pollution is reshaping urban economics. By 2035, if conditions remain unchanged:

Premium neighbourhoods in polluted zones may see value stagnation

Families will increasingly migrate to clean-air microclimates

Investors will prefer land and homes in foothills, coastal regions, and forest-edge communities

Clean-air zones will become the new luxury real estate corridors

Cities don’t collapse due to pollution — but they lose talent, health, and desirability, which is far more damaging over time.

7. What immediate steps can citizens take to reduce pollution exposure?

Citizens can protect themselves by:

Tracking daily AQI and adjusting outdoor activity

Avoiding morning outdoor workouts during winter

Using masks during high pollution days

Installing basic indoor air purifiers

Supporting EV adoption

Reducing personal vehicle usage

Planting native tree species around homes

These steps don’t solve the systemic problem, but they reduce individual health risks significantly.

8. What long-term actions must policymakers take to address Delhi’s pollution crisis?

Delhi’s pollution crisis will not be solved by seasonal bans or temporary emergency measures. Policymakers must focus on:

Electrifying public transport

Creating dust-free construction ecosystems

Protecting and expanding wetlands

Restoring the Yamuna floodplain

Strictly regulating industrial emissions

Improving waste management systems

Designing low-emission neighbourhoods

Prioritising land regeneration as the first line of defense

This is not a “winter issue” but a year-round systems design challenge.

9. How does climate change influence Delhi’s pollution levels?

Climate change worsens pollution by:

Increasing heat island intensity

Reducing wind flow

Changing rainfall patterns

Prolonging dry spells

Strengthening temperature inversions

A warmer, drier city traps pollution longer. Delhi’s climate trajectory will amplify pollution unless ecological buffers are restored.

10. What will Delhi look like in 2035 if nothing changes?

If the current pattern continues, Delhi in 2035 will likely experience:

Permanent mask culture

Higher childhood asthma rates

Shrinking talent pools

Increased migration to cleaner states

Stagnant property values in polluted zones

Greater economic costs from healthcare

A generation growing up without outdoor childhoods

But if we choose differently — if we redesign mobility, protect land, restore rivers, and regenerate soil — Delhi can become a city that breathes again.

The choice is not scientific. It is political, cultural, ecological, and deeply personal.

WHAT WE MUST DO NOW

Citizens

Track AQI

Avoid outdoor workouts in winter mornings

Use masks when needed

Support EV adoption

Plant local trees

Demand better land-use policy

Policymakers

Strengthen ecological buffers

Enforce clean construction

Restore wetlands

Invest heavily in EV public transport

Plan climate-resilient neighbourhoods

Investors & Land Owners

Bet on clean-air geographies

Prioritise regenerative land

Understand that soil health = property value

Move beyond hyper-urban density

The future of real estate: clean air + strong soil + living ecosystems.

THE AIR WE BREATHE TOMORROW IS SHAPED BY THE LAND WE PROTECT TODAY

This Delhi pollution analysis is not only an environmental report. It is a mirror.

It shows:

What we have allowed

What we have ignored

What we have broken

What we can still rebuild

Delhi stands at a crossroads.

One path leads to a city that survives. The other leads to a city that thrives.

A city that chokes. Or a city that breathes.

A city where children cough. Or a city where children climb trees and feel the winter sun without fear.

We are writing Delhi’s 2035 story right now — through every decision about land, water, soil, air, transport, policy, real estate, and design.

What we choose today becomes the air our children breathe tomorrow.

The Sky That Wouldn’t Lift: How Air Pollution in Delhi Redefined Land, Life, and Survival

THE MORNING WHEN THE SKY GREW HEAVIER THAN TRUTH

The morning of 22 November 2025 began like a confession.

Not the kind spoken aloud. The kind whispered by land. By air. By the soil itself.

When I stepped out to breathe, the city refused to let me.

A burnt-orange glow smudged itself across the horizon. The sky didn’t look like dawn. It looked like a warning. It looked like the city was slowly suffocating and still pretending to go to work on time.

I opened my window, and the air felt… dense. Dense with smoke. Dense with chemicals. Dense with a truth Delhi has been trying to outrun for decades.

On 22 November, Delhi’s average AQI hovered around 364–400, with multiple stations breaching 425–445. Mundka touched 442, Jahangirpuri and Bawana touched 428–429. This wasn’t weather. This wasn’t haze. This was air pollution in Delhi in its most honest form.

But numbers rarely capture reality. Breath does.

And on this morning, every breath told me the same thing:

We are inhaling the future we are creating.

THE DAY DELHI STOPPED BREATHING — 22 NOVEMBER AQI, UNFILTERED

I’ve lived long enough with land to recognise a pattern before the world calls it one. I’ve watched soil crack, rivers thin, hills erode, forests whisper their losses.

And I’ve watched Delhi’s sky follow the same trajectory as its soil.

On 22 November:

The average AQI was in the “very poor” to “severe” zone.

PM2.5 peaked to 280–300 µg/m³ in several pockets — nearly 20 times India’s allowable standard and 100 times the WHO’s safe limit.

Over 16 days out of 21 in November, Delhi remained in the “very poor” category.

What shocked me was not the number. It was how normal it felt.

That is the tragedy of air pollution in Delhi — the normalization of slow, invisible violence.

We’ve turned toxic air into an annual routine:

Standstill winds in November

Inversion layers trapping pollutants

High traffic density

Construction dust

Industrial emissions across NCR

Degraded soil turning into airborne dust

Stubble burning drifting down from Punjab & Haryana

These forces come together like clockwork — the Calendar of Choking, I often call it.

And Delhi follows its cruel rhythm:

September: humidity traps pollutants October: stubble burning begins November: winds disappear December: inversion peaks January: fog + trapped PM2.5 February: mild relief March–August: the only months the city can pretend it’s breathing

This is not a season. This is a system.

And on 22 November, that system tightened its grip.

“IF YOU CAN LEAVE, LEAVE.” — THE MOST HONEST MEDICAL ADVICE OF OUR TIME

There is one sentence that has echoed more loudly than any policy announcement:

Doctors from AIIMS, Fortis, Max, SGR — all saying the same thing. I’ve spoken to pulmonologists who say:

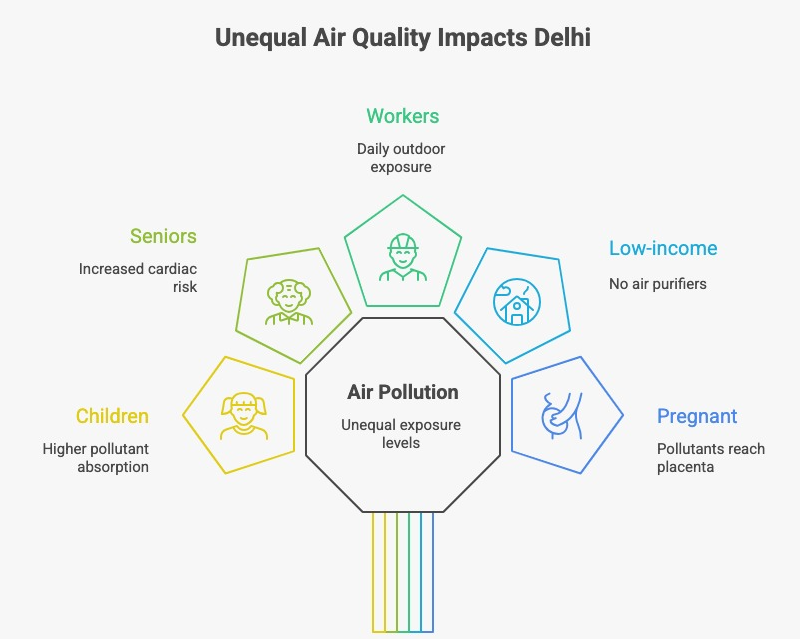

Children are inhaling toxic air equal to 20–25 cigarettes/day

Seniors show sudden drops in oxygen saturation

Cardiac patients face heightened stroke risk

Pregnant women are experiencing pollutant transfer to the placenta

Teenagers show early signs of reduced lung elasticity

A doctor friend told me, “Kushal, this is not an air crisis. This is a population-level lung injury.”

But here’s the truth I’ve learned walking through both forested lands and concrete cities:

Most people cannot leave.

The privilege of clean air is becoming the new class divide.

THERE ARE THREE TYPES OF PEOPLE IN DELHI:

1. Those who can leave

They get into cars, drive to Himachal, Uttarakhand, Goa. Their lungs reset.

2. Those who can sometimes leave

People like me, who work remotely, run businesses, or have farm retreats. We oscillate between survival and responsibility.

3. Those who cannot leave

The largest group — the backbone of the city. Drivers. Teachers. Students. Retail workers. Small businesses. Delivery agents. Security guards. People who inhale Delhi because they must live in Delhi.

For them, air pollution in Delhi is not a headline. It is their morning breakfast, afternoon fatigue, evening breathlessness, night-time cough.

It is the city entering their lungs faster than opportunity enters their lives.

THE CRUEL SCIENCE OF WHAT WE ARE BREATHING

I’ve never been intimidated by data. I’ve been intimidated by what the data means for human life.

On 22 November, Delhi inhaled:

PM2.5 — The assassin you cannot see

These ultra-fine particles seep into:

your lungs

your bloodstream

your heart

your brain

even foetal tissue

They are microscopic violence.

PM10 — The dust of broken land

This is where soil degradation becomes air degradation. When soil dries, cracks, erodes — it becomes PM10. And with enough friction, PM10 becomes PM2.5.

NO₂ & SO₂ — The respiratory trigger duo

Produced by vehicles, industrial combustion, and power plants.

Ground-level ozone — The unexpected enemy

Created when sunlight reacts with pollutants. Not visible. But dangerous.

Black carbon — The residue of our rush

From diesel, biomass, and unregulated combustion.

The (CPCB Dashboard) looked like a battlefield. But here’s the real problem:

The body doesn’t forget. It stores every breath. It remembers every winter. It accumulates every microgram.

THE PEOPLE TRAPPED INSIDE THE CITY’S AIR-CAGE

I want to speak directly about this, without filters.

When I work with land, I ask: Who does this land serve? Who will it protect? Who will it fail?

In Delhi’s case, here is the brutal truth:

Children suffer first.

Small airways + high breathing rate = maximum absorption.

Seniors suffer silently.

Their lungs do not regenerate.

Outdoor workers are the city’s frontline victims.

Delivery riders Hawkers Cab drivers Traffic police Construction workers

They breathe for 10–14 hours outdoors.

Low-income households suffer disproportionately

No purifiers No insulation No alternate home No financial cushion

Women suffer uniquely

Indoor pollution doubles during winter. Outdoor hazard adds a second layer.

Students suffer invisibly

Brain fog Fatigue Reduced cognitive performance Long-term anxiety patterns

And so the question becomes:

When air becomes privilege, what becomes of equality?

WHAT 22 NOV TELLS US ABOUT OUR NEXT 10 YEARS

I’ll say it plainly, because real estate and land development without honesty is just commerce:

If the current trajectory continues, Delhi will be the world’s least breathable mega-city by 2035.

Here is the future Delhi is walking toward:

1. A 6-month pollution season

September to February — half the year in toxic air.

Because land and air are not separate systems. They are one conversation.

SECOND HOMES & CLEAN-AIR MIGRATION — THE QUIET REVOLUTION

I never set out to build luxury. I set out to build sanctuaries. Spaces where land still remembers how to breathe.

But something changed over the last four years.

When families call me now, they say things like:

“My son can’t inhale this air anymore.” “My father’s heart condition gets worse every November.” “My daughter’s cough doesn’t go away.” “We need somewhere to escape during winter.”

The second home is no longer a holiday idea. It has become respiratory insurance.

Why second homes matter in this crisis:

1. Temporary relocation saves lungs

Two weeks in clean environments reverse inflammation.

2. Children’s bodies recover faster

Their lungs expand, oxygenation improves, sleep resets.

3. Productivity rises

Foggy thinking, fatigue, emotional irritability — all drop in fresh-air zones.

4. Medical dependency lowers

Fewer inhalers, fewer emergency visits.

5. Mental health rebalances

Because clean air is not just oxygen. It is clarity.

6. Long-term wealth grows

Regions with forests, soil health, and wind corridors will flourish.

These are no longer travel spots. They are breathing corridors.

LAND IS WHERE THIS ENTIRE STORY BEGINS — AND WHERE IT WILL END

I say this not as a developer, but as someone shaped by soil:

Air pollution in Delhi is not an air problem. It is a land problem.

Look beneath the smog:

Degraded soil becomes airborne dust

Dead trees remove natural filters

Broken Aravalli ridges allow desert winds to enter

Urban heat islands intensify PM concentration

Wetlands lost → no natural cleansing

Overbuilt surfaces → no wind flow

I’ve walked through lands in Sariska where the wind still carries purity. Through forest corridors in Chail where mornings are crisp. Through villages in Goa where trees stand like guardians of life.

All these places taught me the same truth:

The air is just the messenger. The land is the message.

If soil collapses, air collapses. If forests collapse, lungs collapse. If water systems collapse, immunity collapses. If land loses its breath, cities lose their future.

WHAT INDIA MUST FIX — A LAND-FIRST FRAMEWORK

If we truly want to heal air pollution in Delhi, here is what we must do:

5. Can children recover lung capacity after breathing Delhi’s air?

Partial recovery is possible with extended exposure to clean air.

6. Which regions provide refuge from air pollution in Delhi?

Sariska, Uttarakhand, Himachal, Goa interiors.

7. How is soil linked to air pollution in Delhi?

Degraded soil → dust → PM10 → PM2.5.

8. Will air pollution in Delhi worsen over the next decade?

Yes, unless land-first action begins immediately.

9. Are air purifiers enough?

They help indoors but cannot replace outdoor clean air systems.

10. Can land investment protect families from air pollution in Delhi?

Yes — land with natural vegetation, altitude, or forest adjacency acts as a wellness buffer.

THE LAND REMEMBERS WHAT WE FORGET

Standing in the forests of Sariska last week, I watched the wind move through the trees like a prayer. And I realised something profound:

Cities chase speed. Land chases balance. Air carries the consequences of both.

Delhi’s air is telling us a truth we’ve ignored for too long:

We cannot heal the sky until we heal the soil. We cannot protect our lungs until we protect the land. We cannot build a future if the future cannot breathe.

On 22 November, Delhi didn’t just choke. It reminded us that breath is borrowed — from land, from forests, from ecosystems smarter than us.

My message is simple:

Choose land that breathes. Choose soil that regenerates. Choose spaces where your children can inhale their own future.

Because the land remembers. The air reveals. And legacy is built only where life can breathe.

THE GREAT LAND RESET (2025–2030): WHY I BELIEVE LAND INVESTMENT IN INDIA IS ENTERING ITS MOST POWERFUL DECADE

Land has been my teacher for more than two decades. And if there’s one thing the soil keeps reminding me, it’s this:

Land remembers. Land heals. Land outlives us.

But in 2025, I noticed something new — something I haven’t seen in all my years working in forests, hills, coasts, and rural belts across the country.

Land suddenly stopped behaving like an asset. It started behaving like a signal.

A signal that families were tired. Cities were choking. The climate was shifting. And people were finally looking at land not as a transaction, but as a life-support system.

I felt this transformation everywhere I walked:

In Goa, when a family office offered 4× market price for a barren hillside I wasn’t even planning to sell.

In Sariska, where three HNIs tried to corner the same 22-acre forest-edge parcel — not for villas, but for long-term ecological security.

In Himachal, where a rocky slope with no road, no water, no power sold in eleven days.

These moments made one thing clear to me:

A new era of land investment in India has begun — quieter, wiser, more ecological, and deeply personal.

Before I take you into the heart of this shift, let me ground you in the basics.

LAND IN 60 SECONDS — HOW I SEE IT TODAY

After years of walking land, studying policy changes, and observing migration patterns, here’s the simplest way I can explain what’s happening:

DDA, BDA, CIDCO, GMADA — everyone is monetising at scale.

All this together is creating the strongest foundation I’ve ever seen for long-term land investment in India.

But the turning point of 2025 wasn’t just economic — it was personal.

WHAT I SAW ACROSS INDIA (MY 14-MONTH PATTERN)

Across Goa, Sariska, Bicholim, Kufri, Chail, Karnataka, Vidarbha, and Uttarakhand, I met buyers with completely different intentions compared to the last decade.

Here’s the pattern I couldn’t ignore:

1. People aren’t buying to build anymore

They’re buying for:

Clean air

Quiet

Water security

Ecological continuity

A backup life

A return to soil

2. HNIs are quietly exiting built real estate

Raw land feels safer, purer, uncorrelated. I see this every week.

3. Families want legacy, not leverage

They want land their grandchildren can inherit, not apartments their grandchildren will demolish.

4. NRIs want emotional return

Soil > structures. Roots > rentals.

5. Everyone wants resilience, not speculation

This is the biggest shift I’ve witnessed in land investment in India.

People are not chasing appreciation. They are chasing anchoring.

But this shift didn’t happen alone. Policy played a huge role.

THE POLICY RESET NOBODY IS TALKING ABOUT

2025 quietly became the most consequential year for land governance.

Let me break down the three biggest changes I tracked personally:

In Mihin Laling vs State of Arunachal Pradesh, the Court ensured states couldn’t bypass fair compensation rules. For investors, this means predictability along infrastructure corridors.

THE ECOLOGICAL TRUTH: LAND IS NOW A HEALTH INSTRUMENT

For decades, we treated land as a commodity. 2025 forced us to see land as a health asset.

This is the slow-compounding zone of land investment in India.

THE 2025–2030 LAND APPRECIATION CYCLE (MY VIEW)

2025–26 — Reset Phase

Digitisation + title clarity + auction benchmarks.

2026–27 — Ecological Premium Phase

Land with water, trees, and microclimates appreciates faster.

2027–28 — Migration Wave

Families shift away from polluted metro regions.

2028–30 — Scarcity Era

Forest-edge, water-secure, and low-density land becomes gold.

MY PERSONAL FRAMEWORK FOR BUYING LAND (WHAT I FOLLOW)

1. Purpose before plot

Clarity brings the right land to you.

2. Study the soil, not the brochure

Soil truth > marketing fiction.

3. Verify every legal angle

Always use official portals.

4. Follow water

Water decides destiny.

5. Understand regional intention

Some land wants to be forest; some wants to be farm.

6. Think in decades, not years

Land rewards slowness.

7. Build an ecosystem, not a structure

Structures depreciate. Landscapes appreciate.

8. Leave the land better than you found it

This is the highest form of wealth.

FAQ

1. Is land investment in India safe in 2025–2030?

Yes — if you buy with clean title, correct classification, and verified documents. Policies, digitisation, and record reforms have significantly improved safety for land investment in India. Always verify mutation entries, revenue records, and ownership history using official state portals before purchase.

2. Can NRIs legally buy land in India?

NRIs can buy non-agricultural land freely, but agricultural land purchase depends on state rules. Some states restrict agricultural land to only agriculturists. Always verify the local law before planning any land investment in India, especially if you are an NRI purchasing agricultural parcels.

3. Does farmland appreciate slower than real estate?

No. In many regions, farmland has outperformed urban real estate due to scarcity, water access, and ecological value. With climate stress rising, well-located farmland is becoming a prime category of land investment in India, especially for long-term wealth builders.

4. What documents are required for land purchase?

Key documents include: Sale deed, mother deed, mutation records, 7/12 extract or Jamabandi, encumbrance certificate, survey map, classification certificate, RTC, and tax receipts. Verifying these carefully is essential for secure land investment in India.

5. How do I know if land is good for agriculture or regeneration?

Check soil carbon %, water table data, vegetation type, previous land use, and nearby cultivation patterns. Government soil portals and CGWB groundwater reports provide reliable reference points. Good soil and stable water significantly increase the long-term value of land investment in India.

6. Is buying forest-adjacent land legal?

Yes, as long as the land is revenue land (private) and not part of protected forest, reserve forest, wildlife sanctuary, or eco-sensitive zone. Always cross-check boundaries using Forest Survey of India maps. This is a crucial step in safe land investment in India.

7. What is the best size to start with?

Start with what is manageable — even 0.5 to 1 acre is enough for regenerative value creation. The key to land investment in India is not the size, but the clarity of purpose and the ecological potential of the land.

8. Which is better — buying land or buying property?

Land offers sovereignty, control, permanence, and ecological abundance. Property offers convenience but depreciates faster and depends on market cycles. For long-term stability, land investment in India remains a stronger, more resilient asset compared to built real estate.

9. How long should I hold land for best returns?

Ideal hold time is 7–15 years. Land compounds quietly but powerfully across ecological cycles. The longer you hold — and the more you regenerate — the higher your outcomes in land investment in India.

10. Can land generate passive income?

Yes — through agroforestry, plantations, eco-tourism, homestays, water credits, carbon credits, and nature-linked revenue models. As India expands climate-linked markets, passive income from land investment in India will grow significantly.

THE LAND REMEMBERS

Land doesn’t respond to speculation. Land doesn’t move with markets. Land doesn’t care about trends.

CARBON CREDIT IN INDIA 2025: THE NEW WEALTH HIDDEN IN OUR SOIL

THE ECONOMY INDIA NEVER SAW COMING — UNTIL NOW

There comes a moment in a nation’s journey when wealth stops coming from factories, markets, and balance sheets—and begins rising quietly from land, forests, and soil. India is standing in that moment right now.

Every industry is measuring its emissions. Every corporate board is recalculating the cost of carbon. Every policymaker is assigning a financial value to air we pollute and to land we restore.

And without fanfare, without noise, without celebration… a new economy is being born.

This new economy is called carbon credit in India.

You cannot touch it. You cannot see it. But it is shaping:

how factories operate,

how land is valued,

how forests are protected,

how investors behave,

and how India will grow in the next 25 years.

For decades, India treated emissions as environmental issues. Now they are financial assets and liabilities. For decades, India treated forests as scenery. Now they are becoming carbon banks. For decades, rural India was left out of the wealth conversation. Now it may become the center of a new economic revolution.

But here is a truth most people are not ready to hear:

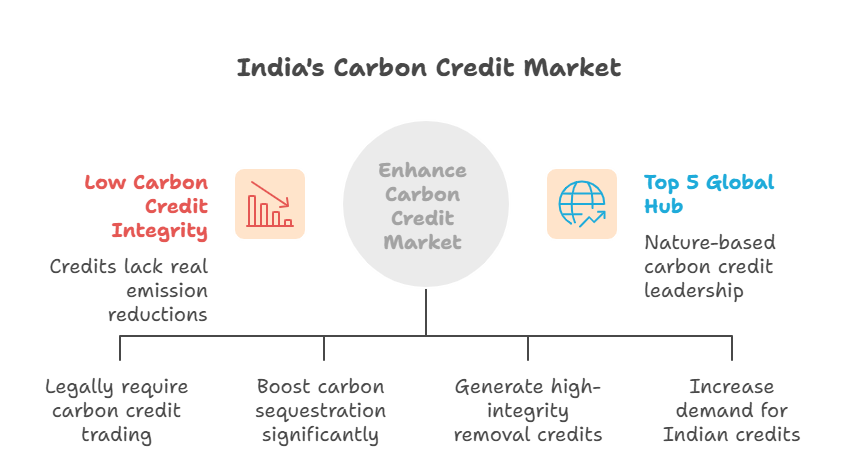

Carbon credit in India is not simply a climate policy. It is a land policy. It is a soil policy. It is a future policy.

And this is where our story begins.

INDIA’S QUIET REVOLUTION: THE DAY CARBON BECAME LAW

For years, the phrase carbon credit in India floated around in climate reports, sustainability conferences, and corporate presentations.

Without baselines, no carbon credit in India can be issued.

(4) Community rights are non-negotiable.

FPIC (Free Prior Informed Consent) is mandatory under global rules.

(5) India’s Article 6.2 market will open premium opportunities.

High-integrity projects can sell credits globally.

THE 2030 VISION: WHAT INDIA MUST BUILD

For carbon credit in India to unlock its full potential, we need:

→ A unified national registry

Transparent, digital, traceable.

→ Strong soil carbon methodologies

India’s soil is degraded; restoring it is a trillion-rupee opportunity.

→ Ecosystem-first, not plantation-first design

Monocultures destroy biodiversity.

→ Fast but fair approvals

Community rights + scientific verification.

→ Financial literacy for carbon farmers

Rural India needs access, not complexity.

THE PHILOSOPHY OF CARBON

When I walk through a forest in Sariska… When I stand on a ridge in North Goa… When I sit by a stream in Himachal… I realise one thing:

Carbon is not a villain. Carbon is memory.

It remembers:

the soil you restored,

the forest you protected,

the land you honoured,

or the land you destroyed.

Carbon credit in India is not the point. Carbon consciousness is.

The air is only the messenger. The soil is the message. And the land is the witness.

The future of wealth will not come from what we build above ground— but from what we rebuild below it.

If pollution taught India one hard truth, it is this:

Wealth belongs to those who think ahead.

And if carbon credit in India teaches us anything, it will be this:

The future belongs to those who restore, not exhaust.

The smartest investment any Indian family can make today?

Land that regenerates. Land that heals. Land that stores carbon, water, life, and legacy.

Not because carbon credit in India will pay for it— but because your children will breathe because of it.

FAQs

1. What is carbon credit in India and how does it actually work on the ground?

Carbon credit in India is a measurable, verifiable unit that represents one tonne of reduced, avoided, or removed CO₂ emissions. But unlike many countries that adopted carbon markets decades ago, carbon credit in India is designed as a dual system:

A. Compliance Carbon Credits

These are mandatory for India’s largest emitting industries. Under India’s Carbon Credit Trading Scheme (CCTS), sectors like:

cement

steel

power

fertiliser

petrochemicals

must reduce their emission intensity every year. If they cannot meet targets, they must buy carbon credit in India to cover the gap. If they overachieve, they earn carbon credits.

This makes carbon credit in India a legally backed financial instrument, not just a climate idea.

B. Voluntary / Nature-Based Carbon Credits

These are created from:

forests

wetlands

mangroves

regenerative agriculture

grassland restoration

soil carbon projects

These credits are purchased voluntarily by companies aiming for:

net-zero emissions

ESG goals

carbon neutrality

This side of carbon credit in India is especially powerful because it rewards restoration, not just prevention.

Together, these two markets show that carbon credit in India is not just about counting emissions—it is about revaluing the country’s land and ecological systems.

2. Why is carbon credit in India becoming so important now?

Three forces have collided to make carbon credit in India a national priority:

1. Legal Pressure (Domestic)

With the October 2025 rules, industrial decarbonisation is now enforced by law. Companies cannot ignore emissions anymore. They must buy carbon credit in India to stay compliant.

2. Economic Pressure (Global Trade)

Europe’s CBAM (Carbon Border Adjustment Mechanism) will tax Indian exports with high carbon footprints starting 2026. If exporters don’t reduce emissions, they must buy certified carbon credits. This makes carbon credit in India essential for protecting India’s export economy.

3. Ecological Pressure (Land & Climate)

India’s soil is degrading, forests are fragmenting, and climate impacts are intensifying. Regenerative land-use practices that generate carbon credit in India also improve:

soil health

water retention

biodiversity

microclimates

This makes carbon credit in India not just a compliance tool—but a land-healing tool.

3. Who can actually earn money from carbon credit in India?

This is one of the most misunderstood questions.

Here is the real answer:

A. Industrial Entities

If industries reduce their emissions beyond mandated limits, they earn compliance credits.

B. Large Landowners

Owners of:

degraded land

grasslands

forested land

agricultural land

…can participate in nature-based carbon projects.

C. Farmers (Individually or as Groups)

Farmers can earn carbon credit in India through:

agroforestry

cover cropping

regenerative agriculture

soil carbon enhancement

low-tillage practices

A single farmer may earn modest revenue, but farmer-producer companies (FPCs) and community clusters can earn significant value.

D. Tribal Communities

Communities managing forest landscapes under FRA (Forest Rights Act) can generate forest-based credits.

E. Developers (Eco-centric)

Developers building:

regenerative resorts

eco-villages

forest communities

land restoration projects

…can embed carbon credit in India into long-term land valuation.

F. Investors

ESG funds and nature-based funds can invest in land restoration and earn returns from carbon credits.

In short, anyone who restores land or reduces emissions can participate in carbon credit in India—but only through verified, transparent, long-term projects.

4. Are forest projects reliable for generating carbon credit in India?

Forest projects are powerful—but only when designed correctly.

They must follow high-integrity rules:

1. Additionality

The forest must grow or revive only because of the project—not because it was naturally happening anyway.

2. Permanence

The carbon must stay locked for decades (usually 20–40 years). If forests burn, are cut, or degrade, credits can be revoked.

3. Leakage Control

You cannot stop deforestation in one area if it shifts deforestation to another area.

4. Monitoring & Verification

Credible forest-based carbon credit in India requires satellite monitoring, drone assessments, growth plots, and third-party audits.

5. Community Consent (FPIC)

Forest carbon projects cannot proceed without tribal rights, community consent, and benefit sharing.

If these conditions are met, forest-based carbon credit in India becomes one of the most valuable climate assets in the world.

5. How is the price of carbon credit in India determined?

There is no single fixed price. Price depends on what type of credit you generate:

A. Compliance Credits

These will be governed by:

supply & demand

industry performance

national targets

regulatory caps

economic cycles

Initial price may be lower, but as targets tighten, value will rise.

B. Voluntary Credits

Voluntary carbon credit in India is priced by:

project type (forest > soil > renewable energy)

carbon quality

permanence guarantees

monitoring intensity

biodiversity co-benefits

location (India is rising as a premium geography)

High-integrity nature credits globally sell for ₹800–₹3,500 per tonne, depending on quality.

Over time, as rules strengthen, the price of carbon credit in India will rise significantly—especially for land-based removal credits.

6. Can farmers realistically earn meaningful income from carbon credit in India?

Yes — but only when certain conditions are met.

For farmers, carbon credit in India becomes profitable when:

✔ They work in groups.

Farmer-producer companies or collectives earn more than individuals.

✔ They use regenerative practices.

These include:

multi-layer farming

agroforestry

organic composting

reduced tillage

cover crops

watershed improvement

These improve soil carbon, which becomes measurable credit.

✔ They have long-term support.

Carbon credit in India requires baselines, audits, MRV systems, and annual reporting.

Farmers need technical partners.

✔ They integrate trees (agroforestry).

Trees pull carbon from the air into biomass. This is one of the most powerful pathways for farmers.

If structured properly, carbon credit in India can add ₹15,000–₹45,000 per acre annually for cluster-based agroforestry projects, depending on methodology and species mix.

7. Is carbon credit in India internationally recognised?

Yes — and this is where India’s future becomes exciting.

Under Article 6 of the Paris Agreement, countries can trade carbon credits internationally. India is building:

a national registry

internationally aligned methodologies

market integrity frameworks

This makes high-integrity carbon credit in India eligible for:

international buyers

global compliance markets

carbon removal portfolios

export under bilateral agreements

India can become a top-5 global supplier of nature-based credits between 2027–2035 if the ecosystem is built correctly.

8. Can every land parcel produce carbon credit in India?

No — and this is the misconception causing the most confusion.

Land must meet specific criteria:

A. It must have a measurable baseline.

You cannot create carbon credits from what you cannot measure.

B. It must show improvement.

Soil must regenerate. Trees must grow. Ecosystems must strengthen.

C. It must be protected for 20–30 years.

Short-term projects are not eligible.

D. It must avoid double registration.

No project can sell the same carbon twice.

E. It must not harm biodiversity.

Monoculture plantations will be rejected under new rules.

In short: only scientifically designed, long-term regenerative projects can generate carbon credit in India.

9. What is the long-term future of carbon credit in India (2025–2035)?

The future of carbon credit in India is enormous — but not in the way most people think.

Here is the real future:

1. Carbon → Water → Soil → Biodiversity

Regeneration will become a multi-benefit economy. Carbon will be the entry point, not the end point.

2. Rural India will become a climate services provider.

Communities managing forests, farms, and wetlands will earn consistent revenue.

3. The most valuable carbon credit in India will be “removal credits.”

Credits created by:

forests

mangroves

grasslands

soil regeneration

wetlands

These will dominate the premium markets.

4. Land value will rise based on ecological performance.

Healthy land will become wealth. Degraded land will become liability.

5. India will become a global carbon exporter.

With one of the world’s largest restoration potentials, India can lead nature-based markets.

The next decade is not about carbon credit in India alone. It is about redefining the relationship between land, livelihood, and legacy.

10. Why is carbon credit in India fundamentally a land-based system?

Because carbon does not live in the sky. It lives in the soil. In the roots. In the forests. In the grasslands. In the wetlands. In the mangroves.

Air pollution is only the surface symptom. Land degradation is the root cause.

And that is why:

Fix the land → Fix the carbon → Build the future.

This is the philosophy behind carbon credit in India. It is not about offsets. Not about trading. Not about finance.

It is about healing India’s land — slowly, honestly, regeneratively.

When the land heals, carbon settles. When carbon settles, climate stabilises. When climate stabilises, societies thrive.

This is why carbon credit in India is not merely a market.

It is a mirror. It reflects the health of our ecosystems and the wisdom of our decisions.

AIR POLLUTION IN DELHI 2025: WHEN A CITY CANNOT BREATHE, WHERE DO ITS PEOPLE GO?

There comes a moment in every crisis when a city stops blaming the weather, the farmers, the government, or even fate—and starts accepting that something has fundamentally broken. Right now, that moment is unfolding in the National Capital Region.

Every morning, millions open their windows only to shut them again instantly. The air smells of burnt smoke, chemicals, and dust. The horizon disappears. The sky becomes a single grey sheet. The throat burns before breakfast. Children cough before school. Traffic lights hang in a yellow haze.

This is not fog. This is not winter. This is air pollution in Delhi.

Doctors across major hospitals—from AIIMS to Sir Ganga Ram—have started saying something no one in Delhi ever expected to hear:

“If you can leave Delhi for a month… leave.”

But here is the truth that rarely gets spoken aloud:

Most people cannot leave.

Most people do not have a second home to escape to. Most people do not have parents in Himachal or land in Uttarakhand. Most people cannot pack their life into a suitcase and drive towards clean air.

Delhi has 3 classes of residents during peak pollution:

Those with second homes or rural roots

People who can temporarily move to:

Himachal

Uttarakhand

Goa

Rajasthan outskirts

Ancestral homes in villages

Farmhouses outside NCR

Those with remote jobs or flexible businesses

Founders, freelancers, consultants who can work from anywhere.

Those who have no choice

Teachers Drivers Office workers Security guards Delivery agents Small business owners Students Elders People who run shops People living in congested neighbourhoods

This last category—millions of them—have to breathe the city’s air, no matter what.

This is the group that suffers the worst consequences of air pollution in Delhi.

PM2.5: toxic micro-particles smaller than 2.5 microns

PM10: coarse dust particles

SO2: from coal burning

NOx: from vehicle emissions

Ammonia: converting to secondary PM

Ozone: created by sunlight + pollutants

Black carbon: from diesel and biomass burning

Do you know what PM2.5 does?

It enters:

lungs

bloodstream

heart

placenta

foetal organs

brain

The European Association for the Study of the Liver even connects PM2.5 to metabolic disorders—but that’s another story.

Now imagine all this multiplying during:

low winds

stubble burning

construction dust

industrial emissions

thermal plants running at winter peak load

Air pollution in Delhi is not an event. It is a metabolic attack.

WHY MOST PEOPLE CANNOT ESCAPE — THE HARDEST TRUTH OF ALL

Out of Delhi’s ~33 million population (Delhi + NCR):

Less than 7–10% have a second home

Less than 4% can work fully remote

More than 70% depend on in-person work

More than 50% live in areas with no air purifiers

More than 40% live in poorly ventilated homes

This means:

When the city chokes, only a fraction can leave.

Millions cannot run from air pollution in Delhi because life pins them to the city:

jobs

schools

hospitals

rent

parents

responsibilities

lack of alternative shelters

And even if someone wanted to leave for 30 days…

Where would they go?

Who will pay the rent for two places?

Who will pay for travel?

Who will move with children’s school schedules?

This is the social truth no report, no doctor, no government plan fully acknowledges.

Air pollution in Delhi divides people: those who can escape, and those who endure.

THE WINNERS ARE THE ONES WHO THINK MONTHS AHEAD

Every year, from September to February, the city becomes a hazard zone. Yet every year, people react—never prepare.

But the families who are winning this struggle against air pollution in Delhi do one thing differently:

They think long-term.

Not in November. Not when AQI touches 450. Not when the child starts coughing.

They think in:

April

May

June

July

When they know that six months later— Delhi will hurt them again.

This is the new logic of urban India:

The smart prepare.

The wise hedge. The long-term thinkers plan for clean-air escape routes.**

Which brings us to a solution almost no one talks about publicly:

SECOND HOMES & LAND BUFFERS — THE ONLY REAL ESCAPE FROM AIR POLLUTION IN DELHI

The concept of second homes in India used to be about:

vacations

status

leisure

But now?

A second home is survival infrastructure.

Why second homes matter during air pollution in Delhi:

(1) They provide seasonal escape

When Delhi hits AQI 400+, families temporarily relocate to:

Himachal (Chail, Kasauli, Shimla outskirts)

Uttarakhand (Binsar, Naukuchiatal, Mukteshwar)

Goa (interior villages, not too coastal)

Rajasthan (Alwar, Sariska, Pushkar outskirts)

These are quieter, greener, cleaner landscapes.

(2) They protect children

Doctors highlight that children lose lung capacity every time they inhale toxic PM2.5. A second home lets parents protect their kids during severe weeks.

(3) They reduce medical risk

A clean-air retreat reduces exposure for:

seniors

patients

pregnant women

asthmatics

(4) They improve mental health

You cannot think, build, or grow while struggling to breathe.

Clean air resets the nervous system.

(5) Long-term appreciation

Eco-rich, low-density towns are rising in value because they are becoming climate buffers.

WHY LAND IS THE REAL SOLUTION – THE KDR LENS

Here is the truth most people miss:

Air pollution in Delhi is not an air problem.

It is a land problem.

Bad land management created:

dust

erosion

degraded soil

waste mountains

dead rivers

concrete sprawl

vanishing green belts

Air is simply the messenger. Land is the root cause.

When soil loses strength, air loses purity.

This is why land becomes the solution:

1. Trees sequester PM and CO₂

2. Forest belts buffer dust and winds

3. Regenerative landscapes repair microclimates

4. Healthy soil traps particulates

5. Rural ecosystems detoxify bodies worn by city air

A second home on land is not luxury. It is a respiratory refuge.

WHAT INDIA MUST DO (A LAND-FIRST FRAMEWORK)

1. Restore soil

Use agroforestry, bio-compost, mulching, wetlands.

2. Stop treating waste like “someone else’s problem”

5. Educate families about seasonal migration patterns

Air pollution in Delhi is predictable.

6. Create clean-air corridors

Tree belts, green highways, wind pathways.

FAQs

1. Why is air pollution in Delhi getting worse every year?

Air pollution in Delhi keeps worsening because the city sits inside a perfect geographical “pollution bowl.” Low winter winds trap pollutants close to the ground, and temperature inversion creates a lid that prevents harmful particles from escaping into the upper atmosphere. Add to this:

Stubble burning across Punjab & Haryana

Construction dust from NCR’s rapid urban expansion

Industrial emissions from Ghaziabad, Sonipat, Faridabad

Vehicle congestion with over 1.2 crore registered vehicles

Thermal power plants in the surrounding belt

Land degradation & soil erosion contributing massive dust loads

Waste burnings at Ghazipur, Bhalswa & Okhla

All of this creates a cocktail of PM2.5, PM10, NOx, SO₂ and black carbon.

Delhi doesn’t have a pollution problem; it has a pollution system, and every winter, the system activates with brutal precision.

2. Is it true doctors are advising families to leave due to air pollution in Delhi?

Yes. Multiple Indian news outlets have quoted pulmonologists, pediatricians, cardiologists, and emergency physicians warning families—especially those with small children, elderly parents, or asthma patients—to temporarily relocate for 2–4 weeks during peak smog periods.

Doctors from AIIMS, Sir Ganga Ram, Max, Fortis, and Apollo have all made similar recommendations. The logic is simple:

During peak smog weeks, PM2.5 is 80–100× higher than WHO’s safe limit.

Children inhale 2× more air per body weight than adults, making them extremely vulnerable.

Seniors and cardiac patients face higher risks of stroke, arrhythmia, and COPD flare-ups.

Pregnant women are warned about risks to foetal development due to polluted air entering the placenta.

Yet, doctors also admit the uncomfortable truth: Most people do not have the privilege to leave the city.

This is where the divide between those who can escape and those who cannot becomes painfully visible.

3. Who is most affected by air pollution in Delhi?

While everyone breathes the same air, the impact is not equal. The highest burden falls on:

Children (0–14 years)

Underdeveloped lungs

Higher breathing rate

Outdoor school exposure

Long-term lung capacity loss

Elderly (65+)

Weak immunity

Higher risk of pneumonia, COPD and heart attacks

Reduced pulmonary resilience

Outdoor Workers

Delivery riders

Cab drivers

Construction workers

Traffic police

Vendors

Security guards

These groups breathe toxic air 8–12 hours daily.

Pregnant Women

Exposure affects foetal lung, heart, and cognitive development.

Asthma & Cardiac Patients

Air pollution in Delhi is a direct trigger for:

hospitalisations

acute attacks

low oxygen saturation

inflammation spikes

The poor suffer the most because they cannot afford air purifiers, sealed homes, or temporary relocation.

4. How can a second home help during air pollution in Delhi?

Second homes were once seen as luxury. Today they are respiratory sanctuaries. They help because:

Temporary escape

Families can relocate for 20–40 days when AQI hits “Severe+”.

Better lung protection

Children and elders get a recovery window from toxic exposure.

Lower medical dependency

Staying in cleaner areas reduces hospital visits for:

wheezing

asthma attacks

breathlessness

migraines

eye/skin irritation

Mental health benefit

Clean air resets the nervous system and reduces stress.

Long-term investment logic

As air pollution in Delhi worsens yearly, demand for second homes in:

Himachal

Uttarakhand

Rajasthan outskirts

Goa

Maharashtra highlands

…keeps rising.

A second home is no longer a vacation asset. It is a clean-air strategy.

5. What is the safest period to stay in Delhi?

Typically, the cleaner months are:

March

April

July (monsoon)

August (monsoon peak)

Air pollution in Delhi spikes during:

October (post-harvest burning begins)

November (low winds + inversion)

December (cold + trapped pollutants)

January (dense fog + stagnant air)

February is transitional.

This predictable cycle is why long-term thinkers plan ahead—for school holidays, remote work, and relocation windows.

6. Can air purifiers solve the problem of air pollution in Delhi?

Air purifiers help inside homes, but they cannot change what is happening outdoors.

Limitations:

Purifiers don’t work in open spaces.

They cannot filter NOx, SO₂ or ozone.

They don’t address micro-leaks in poorly insulated homes.

They cannot stop infiltration when doors/windows open.

The city has only a handful of public purifier towers—too few to matter.

Think of air purifiers as “masks for your home.” Useful, not transformational.

Only land regeneration and environmental systems can solve air pollution in Delhi at its root.

7. Which Indian regions have healthier air compared to Delhi NCR?

Cleaner-air zones include:

Himachal Pradesh

Chail

Shimla outskirts

Solan

Kasauli

Dharamshala

Uttarakhand

Mukteshwar

Naukuchiatal

Binsar

Ranikhet

Rajasthan (Aravalli belt)

Sariska

Alwar outskirts

Pushkar rural belt

Goa (interior villages)

Sattari

Bicholim

Quepem

Maharashtra (Western Ghats)

Lonavala rural

Karjat

Mulshi

These regions have:

lower dust loads

greener microclimates

lower traffic density

healthier soil systems

natural air corridors

This is why second homes in these areas are rising in demand.

8. Is air pollution in Delhi connected to soil degradation?

Absolutely—this is the connection almost no one talks about.

Soil → Dust → PM10 → PM2.5 → Air pollution

When soil dries, erodes, or degrades, the wind lifts it into the atmosphere. Construction waste, barren land, broken riverbeds, and deforested patches become dust factories.

That dust becomes PM10. PM10 breaks into PM2.5. PM2.5 becomes the smog people breathe.

Add Delhi’s massive construction sector + desert winds from Rajasthan + degraded Aravallis, and you get a perfect storm.

The truth is simple:

Air pollution in Delhi is not an air issue. It is a land issue.

Fix the land → fix the air.

9. When does air pollution in Delhi reach its most dangerous levels?

Peak season:

Late October to mid-January

Immediately after Diwali

During cold, windless nights

During heavy fog weeks

When inversion layers trap pollutants close to the ground

This is when:

lungs inflame

oxygen saturation dips

schools close

doctors issue emergency advisories

children stop outdoor activities

This predictable season is why proactive families plan second-home exits well in advance.

FINAL THOUGHT — THE AIR IS ONLY THE MESSENGER. THE LAND IS THE MESSAGE.

When I walk through my projects in the forests of Sariska or the ridges of Goa, the same truth repeats itself:

Nature is not punishing us. Nature is only mirroring us.

Air pollution in Delhi is not a weather accident. It is a land consequence.

The families who will breathe easier in the future are not the ones who bought purifiers… but the ones who bought foresight.

The ones who planned for September. The ones who didn’t wait for October. The ones who invested in land—not as property, but as protection.

Because the air will always tell the truth. And the soil will always remember our choices.

The smartest decision any Delhi household can make today?

Find a second place where your children can breathe. Not because you are running away from Delhi… but because you are running towards life.

CBAM Carbon Tax India 2026 — Beat It with Credits or Pay in Margins

Europe has found a new way to price pollution. By January 2026, the European Union’s Carbon Border Adjustment Mechanism (CBAM) will become a global turning point — the first international carbon tariff in history.

For Indian exporters, it’s not a distant policy. It’s a price tag on every ton of carbon hidden in your steel, cement, aluminium, or fertiliser. For investors and landowners, it’s something else entirely: a once-in-a-generation opportunity to turn land and trees into export-linked carbon currency.

The CBAM carbon tax India 2026 isn’t just about cost; it’s about control — of who pays for carbon, and who gets paid for absorbing it.

Because the same carbon that Europe will tax is the carbon India can capture. And the same policy that erodes exporter margins can build generational land wealth for those who act now.

CBAM in 60 Seconds

Here’s how it works, simplified.

CBAM means that from 1 January 2026, every tonne of steel, aluminium, fertiliser, cement, hydrogen, or electricity entering the EU will be charged a tax equal to the carbon price European producers already pay under the EU ETS. In plain words:

If you emit carbon to make it, you pay to sell it.

Mechanism: importers declare embedded CO₂ → pay tax unless exporter proves it already paid equivalent carbon price at home.

That last clause changes everything. Because India is launching its own Carbon Credit Trading Scheme (CCTS) in April 2026 — just three months before CBAM enforcement begins. If CCTS is recognised, Indian credits could directly offset the CBAM carbon tax India 2026.

Why CBAM Matters for India

India exports billions of dollars’ worth of CBAM-covered products to Europe every year. That trade flow now carries a hidden cost: its carbon intensity.

Indian steel = 2.7 tCO₂ / t. → Excess = 1.3 tCO₂ × ₹7,600 ≈ ₹9,880 per ton in extra CBAM cost.

Multiply that across millions of tons — you get thousands of crores in new liability once the CBAM carbon tax India 2026 begins.

The equity problem

European producers already pay for their emissions; CBAM simply levels the field. But Indian exporters, who operate in a low-price, high-emission environment, will pay more unless they create certified reductions.

That’s where Indian land and carbon credits come in. When exporters buy domestic credits from verified land projects, they not only avoid foreign taxes but also feed capital into India’s soil.

CCTS + CBAM: A Perfect Policy Collision

The Carbon Credit Trading Scheme (CCTS) launching April 2026 gives India its first national carbon price. This is no coincidence — it’s strategic timing.

CBAM goes live January 2026.

India’s CCTS launches April 2026.

Alignment discussions are ongoing under the EU-India Clean Energy Partnership Framework.

If Europe recognises CCTS, exporters that fund domestic credits can deduct that spend from their CBAM carbon tax India 2026 bill.

The exporter offsets the liability; the landowner earns yield. Everyone wins — except the carbon tax collector in Brussels.

That’s how the CBAM carbon tax India 2026 transforms from a penalty into a new profit channel.

Why Land Is the New Carbon Factory

When you own productive soil, you own time.

Each acre of reforested land sequesters between 0.5 and 2 tCO₂ per year, depending on species and water availability. At ₹6,000 per tCO₂, that’s ₹3,000–₹12,000 annual yield per acre.

Multiply that by 1,000 acres → ₹3 – 12 million in yearly carbon income.

The billionaires buying barren land in Rajasthan aren’t speculating on real estate; they’re pre-buying the infrastructure for the post-CBAM world.

And every acre planted today will sell credits tomorrow — just when exporters start bidding for them.

The Carbon Credit Supply Crunch

According to [IEA Carbon Market Outlook 2025], global credit supply may fall 40 % short of demand once compliance markets expand.

India’s case:

Demand 2026 = ~70 million credits.

Supply ≈ 10 million.

Shortfall ≈ 60 million.

Economics 101: Scarcity drives price.

Early registrants in India’s CCTS will hold the cheapest carbon inventory on the planet. By the time the CBAM carbon tax India 2026 matures, those early credits could trade 2–3× higher.

Exporter’s Playbook: From Tax to Strategy

1 · Quantify Your Exposure

Audit Scope 1 – 3 emissions.

Benchmark against EU averages.

Calculate tonnage × EU price = potential CBAM cost.

2 · Build Your Credit Portfolio

Partner with verified land projects under CCTS.

Pre-purchase credits for 2026–2030 delivery.

Negotiate 10-year of-take agreements to lock price.

3 · Reinvest in Land

Convert a portion of profit into carbon-positive real estate.

Treat land as a natural balance-sheet hedge against carbon liability.

Add ₹20 lakh green infrastructure (solar + trees + water credits).

Revenue ₹6 – 8 lakh / year via carbon + solar excess.

15–25 % premium in resale over non-certified homes.

So while industrialists hedge CBAM liabilities, homeowners earn from the same logic.

Each tree planted in your estate is a micro-credit toward the CBAM carbon tax India 2026 economy.

India’s Policy Momentum

India has already notified nine sectors under the Perform-Achieve-Trade (“PAT”) mechanism — these will link into CCTS. The next step: integration with CBAM.

[Financial Express] reported that EU may allow credits purchased in India to offset border tax.

[IEA Data Portal 2025] confirms India’s emission intensity improvement trajectory since 2019.

All signs point to one truth: CCTS will anchor India’s response to the CBAM carbon tax India 2026, keeping capital and credit value within our borders.

Community and Ethics: Carbon with a Conscience

Every policy creates winners and losers. CBAM could concentrate wealth if handled poorly. The solution is designing credit projects that share benefits with local communities.

A ₹50 lakh project that hires village labour for plantation and shares 5 % of credit revenue builds more than carbon stock — it builds trust.

Ethical carbon is also smart carbon: buyers in Europe now pay premium for credits with biodiversity and social impact co-benefits.

That aligns perfectly with KDR’s philosophy — profit rooted in purpose.

FAQs

1 · What exactly is the CBAM carbon tax India 2026? It’s a border carbon tax imposed by the EU from January 2026 on imported goods based on their embedded CO₂. Indian exporters must pay unless they demonstrate equivalent carbon cost domestically.

2 · Why does it target India specifically? It doesn’t target India alone — but India is a major exporter of high-emission goods, so its exposure is significant. Hence the focus on CBAM carbon tax India 2026 preparedness.

3 · Can Indian credits really offset CBAM costs? Yes, if India’s CCTS gets recognition under EU CBAM rules. Negotiations are underway.

4 · When should investors act? Now. Land prices and credit costs will spike after April 2026 once CCTS is live.

₹50 lakh–₹2 crore → direct land for carbon projects.

₹5–10 crore → eco-estate model combining carbon + eco-tourism.

Each path leads to the same outcome — carbon yield that offsets the CBAM carbon tax India 2026.

What to Do This Week

For Exporters:

Run emission audits.

Identify potential credit suppliers in India.

Budget for carbon offset cost per ton.

For Investors:

Acquire land in high-yield zones before prices factor in carbon value.

Partner with verified project developers.

Target issuance before 2026 tax phase.

For Homeowners:

Plant native trees on your property.

Measure and register carbon offsets.

Market your estate as “carbon-positive certified.”