Kushal Dev Rathi on how carbon credit investment in India turns sustainability into a financial opportunity.

Carbon Credit Investment India is quietly shaping a ₹50,000 crore opportunity — and billionaires have already started positioning for it.

Bill Gates owns 2,69,000 acres of American farmland. Jeff Bezos just added 4,20,000 acres in Texas. And Indian billionaires? They’re quietly sweeping up agricultural land across Rajasthan and Maharashtra — often paying prices that make zero sense.

Unless you understand what’s coming in April 2026.

They’re not buying land for wheat or sugarcane. They’re buying carbon factories. Because the next big wealth wave isn’t tech, it’s carbon credit investment in India — a ₹50,000 crore opportunity about to explode when the government’s Carbon Credit Trading Scheme (CCTS) goes live.

In simple terms, companies will pay for every extra ton of carbon they emit. Land that captures carbon becomes income-generating. And those who control it — the billionaires of today and tomorrow — are positioning now.

Here’s what took me six months, 47 land deals, and 142 hours of research to figure out.

CARBON CREDITS IN 60 SECONDS

Government tells Tata Steel: “You can only emit 1 million tons of CO₂.”

One part of me celebrates that carbon credit investment in India finally values environmental assets financially.

But another part worries: Are we creating “carbon barons” while small farmers lose out?

Here’s what I believe:

₹50,000 crore is flowing into land-based carbon projects.

You can:

A) Ignore it → Watch prices rise as billionaires buy up carbon land B) Participate → Invest early, capture value C) Participate thoughtfully → Support projects that help communities

I’m choosing C.

This isn’t about flipping land.

It’s about recognising that the world assigns monetary value to breathable air—and positioning your capital accordingly.

By December 2025: Shortlist properties By March 2026: Acquire land By June 2026: Start certification By Dec 2026: First carbon credits issued

The window closes in 5 months.

FAQs

1. What is carbon credit investment in India?

Answer: Carbon credit investment in India means owning or funding land that absorbs carbon from the atmosphere through trees, forests, or regenerative farming. Each ton of CO₂ captured earns a carbon credit, which can be sold to companies that need to offset their emissions. From April 2026, India’s Carbon Credit Trading Scheme (CCTS) will formalise this into a regulated market worth ₹50,000 crore.

2. How can landowners in India earn carbon credits?

Answer: Landowners can earn carbon credits by planting trees, restoring degraded land, or adopting sustainable farming that increases carbon sequestration. Once certified under global or Indian carbon standards, they receive tradable credits — typically 0.5 to 2 tons of CO₂ per acre per year — which can be sold to polluting industries or exporters facing carbon tax penalties.

3. When will India’s carbon credit market start?

Answer: India’s official Carbon Credit Trading Scheme (CCTS) launches in April 2026. Nine key industries — including power, steel, cement, aviation, and fertilisers — will be required to buy credits to offset emissions. This policy is expected to trigger massive demand for certified carbon projects and raise the value of green land investments.

4. Is carbon credit investment profitable or risky?

Answer: Like any emerging asset, carbon credit investment carries both opportunity and risk. Early investors benefit from high appreciation potential as demand outpaces supply, but should factor in certification costs, regulatory shifts, and liquidity challenges. The key is to invest in well-managed, verified projects rather than speculative land deals.

We’re standing at the edge of the most considerable revaluation of land since the Green Revolution — only this time, it’s not about how much food land can produce, But how much carbon can it capture?

In a few months, India will start paying for clean air — literally.

When carbon gets priced, land gets repriced. And those who understood this early will own not just acres, but the atmosphere’s value itself.

You can ignore it and watch billionaires buy up the future, or you can act — intelligently, ethically, and early.

Because one day, your grandchildren will breathe the air we invested in. And they’ll ask what role you played when the world first started putting a price on pollution.

Land is no longer just an asset. It’s the planet’s balance sheet. Own your part of it — while it still costs less than clean air.

DISCLAIMER

This is educational research and opinion, not financial advice. Carbon credit investment in India involves risks: regulatory changes, certification delays, price volatility, illiquidity, and policy shifts. All projections are estimates, not guarantees. Consult qualified advisors before any investment decision.

The October 11, 2025, crypto crash revealed a fundamental truth about gold, silver land asset investing: while ₹1.58 lakh crore vanished from digital portfolios in hours, these three physical assets held their value—or even gained value. Gold hit ₹1.28 lakh per 10 grams (all-time high), silver surged to ₹1.85 lakh per kg (up 22% in October alone), and land values remained unchanged because they literally can’t be repriced in four hours. This isn’t about crypto being “bad.” It’s about understanding which assets survive panic and which get liquidated by it.

#1 will make you question your entire portfolio. #3 got me blocked by six crypto influencers. #5 is why I’m researching farmland while Bitcoin is “on sale.”

Let’s start with the uncomfortable one.

IMPORTANT DISCLAIMER:All specific investment examples, transactions, property details, and portfolio allocations mentioned in this article are purely hypothetical and used for educational illustration purposes only. They do not represent actual investments, real transactions, or specific recommendations. This content is for educational purposes and should not be construed as investment advice.

1. Liquidity Is Not Your Friend—It’s Your Weapon Against You

October 11, 2025. 2:47 PM.

I’m driving back from a property research visit near the Maharashtra-Goa border when my phone explodes.

Not from land investors. They’re quiet.

It’s acquaintances. People I’ve met at conferences—that guy who kept telling everyone about his Bitcoin portfolio.

“Kushal, what do I do?”

I pull over. Check the news.

Bitcoin: ₹1.02 crore → ₹87 lakh in three hours. ₹1.58 lakh crore wiped out globally in liquidations.

I think about the land investors I know—the ones with coastal properties, farmland holdings, oxygen-positive acreage. None of them are calling. None of them are panicking.

Because you know what? Even if they wanted to panic-sell their land today, they physically couldn’t. Title verification alone takes a minimum of 30 days.

That’s when it crystallizes.

The crypto investors lost ₹15 lakh per Bitcoin in four hours because they could sell at that time. Land investors didn’t lose anything because land doesn’t have a “sell” button at 3 PM on a panic Friday.

Everyone believes liquidity equals safety. It doesn’t. Liquidity is the exact feature that lets the market—or worse, your own panic—liquidate you.

Let me tell you what happened to my father in 1991. He owned gold. His business partner owned stocks. The market crashed. His partner panicked and sold everything at 11 AM, locking in massive losses.

My father wanted to sell his gold too. But he couldn’t. The jeweller didn’t open until 10 AM the next day. By morning, he’d slept on it and calmed down. Kept the gold. That forced eight-hour pause saved him what would be ₹2.5 crore in today’s money.

Here’s the principle that changed how I think about the gold, silver, and land asset strategy:

The Gold Silver Land Asset Trinity: Physical assets that can’t be liquidated—Gold at ₹1.28L/10g, Silver at ₹1.85L/kg, and Land providing generational wealth without margin calls.

If your portfolio can be liquidated in four hours, it will be liquidated BY YOU in four hours of panic. And panic always strikes at the worst possible moment—at the bottom, never the top.

Gold hit ₹1.28 lakh per 10 grams on October 11—an all-time high. But even gold has a natural circuit breaker. You can’t sell it at 3 AM when you’re lying awake panicking. You have to wait till morning. Find a jeweller. Verify purity. Negotiate.

Silver takes even longer. At ₹1.85 lakh per kg, you need to find a bulk buyer. That takes calls, meetings, and verification. The premium over gold is significant—silver has surged 22% in October 2025 alone, driven by industrial demand and safe-haven buying.

Land? Forget about it. Even if someone wanted to panic-sell farmland on Friday afternoon, they physically couldn’t. Title verification alone takes a minimum of 30 days. Then the buyer searches. Then paperwork. That 60-90 day forced hold? That’s not a bug. That’s protection from yourself.

2. “Diversification” Means Nothing If Everything Crashes Together

This is the one that got me blocked by six crypto influencers on X.

Someone posted Friday evening: “But I’m diversified. I own Bitcoin, Ethereum, Solana, and five other altcoins.”

I replied with what I always say: “That’s not diversification. That’s one asset class wearing eight different hats.”

Not a popular opinion. Got blocked within an hour.

On October 11, here’s what happened to that “diversified” portfolio:

Bitcoin dropped 15%. Ethereum fell 21%. Solana and altcoins? Down 35% to 50%. Everything crashed together. That’s called correlation = 1.0. When one goes down, they all go down. That’s not diversification—that’s concentration risk with extra steps.

Now let me show you what real diversification looks like using actual long-term data and understanding the gold silver land asset framework.

Notice something? These three assets don’t move together.

When COVID hit in 2020, stocks crashed 40%. Gold went up 28% that year. Real estate? Stayed relatively stable because you can’t panic-sell an apartment building at midnight.

When the economy booms, stocks soar. Real estate appreciates steadily. Gold might stay flat or dip slightly because nobody needs a “safe haven” during good times.

That’s actual diversification.

Consider a hypothetical portfolio diversified across the gold silver land asset spectrum—some gold for immediate liquidity at ₹1.28 lakh per 10 grams, silver exposure at ₹1.85 lakh per kg offering both safe-haven and industrial demand drivers, and land spread across airport corridors like Noida, agricultural zones in Rajasthan, and coastal properties in Maharashtra-Goa region. On October 11, while global markets hemorrhaged ₹1.58 lakh crore, such a portfolio’s value? Unchanged.

Not because real estate or precious metals are “better” than crypto. Because these values don’t get repriced every millisecond based on Trump’s tweets. They move quarterly, maybe annually. And that slowness—that illiquidity everyone complains about—is exactly what provides protection.

Here’s the test I give everyone: “If Trump tweets something inflammatory at 3 PM, does your portfolio value change by 3:30 PM?”

If yes, you own correlated assets. If no, you might actually be diversified.

Gold passed that test on October 11. The product actually gained value, hitting ₹1.28 lakh per 10 grams—an absolute record. Silver passed—currently at ₹1.85 lakh per kg, trading on industrial demand cycles (solar panels, EVs, electronics), not Twitter sentiment. Land passed—literally cannot be repriced in 30 minutes.

Crypto failed catastrophically.

The lesson: Owning eight different cryptocurrencies isn’t diversification. It’s the same bet made eight times. And when that bet fails, it fails everywhere simultaneously.

3. The Market Doesn’t Care About Your “Long-Term Vision” When It’s Liquidating You Right Now

This is the truth that got me those blocks.

I posted on X after the crash: “Saying ‘I’m a long-term holder’ doesn’t help when the exchange auto-liquidates your position at 3:47 PM.”

Six crypto influencers blocked me within two hours.

But here’s the uncomfortable reality: ₹1.58 lakh crore in liquidations on October 11. These weren’t people who panic-sold. These were people who got force-liquidated by margin calls. Their exchanges closed their positions automatically because they’d borrowed money to amplify their bets.

Their long-term conviction? Didn’t matter. The liquidation bot doesn’t care about your five-year thesis. It cares about your margin level at 3:47 PM. And at 3:47 PM, thousands of “long-term investors” became involuntary sellers at the worst possible prices.

I’ve seen this movie before. 2008. Real estate developers with fantastic projects, prime locations, brilliant long-term vision. Banks foreclosed anyway because they missed three months of EMIs. Vision didn’t save them. Cash flow did.

Here’s what the gold silver land asset approach gives you that leveraged crypto doesn’t: TIME.

If someone owned farmland worth ₹2 crore and the market temporarily valued it at ₹1.8 crore (which they’d never even know unless actively trying to sell), nothing happens. No margin call. No forced sale. No automatic liquidation.

They just… continue owning land. Six months later, it’s worth ₹2.2 crore, and they barely remember there was ever a “dip.”

Similarly, gold at ₹1.28 lakh per 10 grams or silver at ₹1.85 lakh per kg might fluctuate by 2-3% in a day. But nobody forces you to sell at the bottom. You hold physical metal. It sits in your locker. No exchange can liquidate it.

But if someone owns ₹2 crore in leveraged Bitcoin and it drops 15%, the exchange forces a sell at ₹1.7 crore. Long-term vision ends at 3:47 PM on a Friday. Game over.

I once read about a landowner in Sariska who said, “My land doesn’t have a margin call button. That’s not a limitation. That’s the entire value proposition.”

The truth nobody wants to hear: Long-term investing only works if you can survive short-term volatility. Physical assets—the gold silver land asset trinity—let you survive because nobody can margin-call your farmland or force-liquidate your gold at the bottom of a panic.

4. Gold Isn’t Boring—It’s The Only Asset That Behaves Exactly As Advertised

Everyone calls gold boring.

You know what’s exciting? Watching portfolios drop ₹16 lakh in four hours.

You know what’s boring? Watching gold hit ₹1.28 lakh per 10 grams on the same day crypto crashed—an all-time high while everything else burned.

On October 11, 2025:

Bitcoin promised “digital gold”—crashed 15%. Gold promised “safe haven”—hit ₹1.28 lakh per 10 grams, record high.

Which one behaved as advertised?

Since 1971, gold has increased 8% annually on average, comparable to equities and higher than bonds over the same period Gold’s key attributes – 1. Return | World Gold Council. It’s not exciting. It’s not going to 10x in three months. But it does exactly what it promises: preserve value during chaos.

Silver did something even more interesting during the October crash. While Bitcoin hemorrhaged value, silver surged to ₹1.85 lakh per kg—up 22% in October alone. Why? Because silver serves two masters.

It’s a safe haven like gold. When markets panic, people buy it.

But it’s also an industrial metal. Solar panels need it. Electric vehicles need it. Electronics need it. Silver prices jumped from ₹1.51 lakh per kg on October 1 to ₹1.85 lakh per kg by October 13—a 22.52% increase in just two weeks Silver Rate Today (14 October 2025), Silver Price in India – Goodreturns.

Silver wins both ways. Crisis? Safe haven buying. Recovery? Industrial demand. That’s not diversification within an asset—that’s an asset that’s inherently diversified.

Here’s how one might think about positioning in the gold silver land asset framework right now:

Gold at ₹1.28 lakh per 10 grams is expensive historically. Holding existing positions makes sense—it’s doing its job preserving value during chaos. But adding aggressively at all-time highs? That’s chasing momentum, not strategy.

Land? Everyone’s distracted by the crypto crash. Sellers get nervous about “market uncertainty.” This is historically when patient capital with research done and funding ready finds opportunities—not when everyone’s euphoric.

The principle: Boring assets do their job. Exciting assets do whatever they want. Most successful long-term investors choose boring and predictable over exciting and bankrupt.

5. The Best Time To Research Physical Assets Is When Everyone’s Obsessing Over Digital Ones

Friday evening, October 11. Social media explodes.

“Should I buy the Bitcoin dip?” “Is this a buying opportunity?” “Crypto is 15% off—isn’t that a bargain?”

While everyone’s asking about Bitcoin, something else is happening in the physical asset space.

Landowners who were firm on pricing in September are suddenly more willing to have conversations. Properties that seemed overvalued a month ago are back to rational pricing discussions.

Why now?

Because when everyone’s staring at screens watching crypto prices, nobody’s looking at land. And that creates exactly the kind of market condition that favors patient capital with completed research.

The pattern that repeats:

The best time to research the gold silver land asset space is when: (1) Everyone thinks they’re “old economy” and outdated, (2) All attention is on digital/new/shiny things, (3) Prices haven’t yet adjusted to underlying fundamentals.

October 2025 fits this pattern perfectly.

Everyone’s talking about “buying the Bitcoin dip” and “crypto is on sale” and “digital assets are the future.”

Almost nobody’s talking about gold hitting ₹1.28 lakh per 10 grams (all-time high), or silver surging to ₹1.85 lakh per kg (22% up in October), or coastal land appreciation rates of 18-25% with zero volatility.

That’s the signal.

Properties in areas like Maharashtra-Goa coastal corridor, Sariska buffer zones, or Noida airport periphery that were on research lists before October 11? The crash didn’t change the underlying thesis. But it did change some sellers’ psychology.

A property listed at one price in September? Some sellers call now, voices uncertain. “I’m seeing market turmoil. Would you still be interested in discussing?” Translation: negotiating room has opened.

This isn’t about taking advantage. It’s about understanding market psychology. When people see portfolios crashing (even in unrelated asset classes), they get nervous about everything. That nervousness creates temporary pricing opportunities for patient capital.

Here’s the long-term data that shapes research priorities in gold silver land asset allocation:

These aren’t spectacular “to the moon” numbers. But they’re consistent. Predictable. And most importantly, they compound without liquidation events.

Bitcoin might hit higher peaks. But it also crashes 15% in four hours. The psychological cost of that volatility—the sleepless nights, the constant checking, the fear—that has a price too. It just doesn’t show up in CAGR calculations.

For those researching physical assets:

Coastal Maharashtra-Goa properties merit research (oxygen-positive land, AQI averages 35, the health migration thesis with the November AQI crisis coming). These deserve analysis regardless of crypto crashes.

Silver accumulation strategies at current ₹1.85 lakh per kg levels are being considered. Not because anyone’s certain it’ll hit ₹2.5 lakh. Because the supply-demand fundamentals (182M ounce deficit) and industrial trends (solar, EV) make it worth serious analysis.

Expansion opportunities in areas where legal groundwork is already done—places where revenue records are understood, local authorities are known, water tables and title history are verified.

What makes sense to avoid: Rushing. Buying just because “prices are down.” Skipping due diligence. Leveraging. Deploying money needed in the next two years.

The best research happens before crashes, not during them. October 11 didn’t create new opportunities in the gold silver land asset space—it just revealed which research was already done and which capital was already patient.

What October 11 Actually Taught The Market

I’ve spent over two decades researching land and physical assets. You’d think a ₹1.58 lakh crore crash wouldn’t teach anything new. But it did.

Speed destroys wealth as often as it creates it.

The faster you can exit, the faster fear can exit you. On October 11, people could sell crypto in seconds. So they did. In panic. At the bottom. Those who owned assets that required weeks to transact? They were forced to be patient. That forced patience protected them from their worst instincts.

Correlation is invisible until crisis reveals it.

Everyone thought they were diversified holding eight different cryptocurrencies. On October 11, they learned they’d made the same bet eight times. Real diversification means owning assets that respond to different triggers. Gold’s long-term return is driven by economic components balanced by financial components Gold’s key attributes – 1. Return | World Gold Council, not by Twitter sentiment or leveraged trading. Silver responds to both crisis (safe haven) and growth (industrial demand). Land responds to decades, not minutes.

You can’t have long-term vision without short-term survival.

₹1.58 lakh crore in liquidations represented people who had great long-term theses but couldn’t survive short-term volatility. The market liquidated their leverage before their vision could play out. The gold silver land asset framework doesn’t have this problem. Nobody margin-calls farmland. Nobody force-liquidates gold at ₹1.28 lakh when you hold physical metal. Nobody forces sale of silver at ₹1.85 lakh at 3 AM.

Boring assets do exactly what they promise.

Gold promised to preserve value during chaos. On October 11, it hit ₹1.28 lakh per 10 grams—an all-time high. It did its job. Silver promised both safety and industrial demand growth—surged to ₹1.85 lakh per kg, up 22% in October. It did its job. Land promised stability and remained stable because it can’t be repriced in four hours. It did its job.

Bitcoin promised to be “digital gold.” It crashed 15%. One asset class kept its promises. One didn’t.

This isn’t about crypto being “bad” or physical assets being “better.” It’s about understanding what each asset actually does, what risks it carries, and whether typical investors can survive those risks long enough to see returns.

Many people don’t invest in crypto because they know their own psychology. They’d check prices constantly. They’d panic during crashes. That volatility would cost them sleep, which in turn would cost them decision quality, ultimately costing them money.

So the focus stays on assets that move slowly enough to allow clear thinking. Assets that can’t be liquidated at 3 AM during worry spirals are problematic. Assets that force patience because they literally cannot be sold quickly.

Gold at ₹1.28 lakh per 10 grams. Silver at ₹1.85 lakh per kg. Land measured in acres, not apps.

The boring stuff that’s been preserving and building wealth for thousands of years, while “revolutionary” assets come and go.

What Makes Sense Now (Educational Perspective Only)

Let me be absolutely clear. I’m not a SEBI-registered investment advisor. I don’t know anyone’s specific financial situation, goals, risk tolerance, or timeline. What follows is an educational perspective on market dynamics, not advice.

November is 17 days away. For the past five years, Delhi NCR’s AQI has hit 400-500 every November. People have been panicking about air quality for six weeks. By February, they forget. But the health migration thesis—the foundation of my land research—doesn’t forget.

Areas with clean air merit research year-round. The coastal Maharashtra-Goa corridor, the Himalayan foothill regions, and certain peripheral zones around major cities. Not because of crypto crashes. Because demographic and health trends suggest multi-year opportunities.

Some sellers are more open to negotiation now than in September. Market uncertainty creates opportunities for patient capital with research already completed. But nothing gets bought that wasn’t already being researched. Crashes don’t change fundamental analysis—they just change timing.

Emergency liquidity strategies often include some allocation within the gold silver land asset framework. The principle is simple:

Gold at ₹1.28 lakh per 10 grams provides immediate liquidity—convertible to cash within hours if absolutely needed. It’s expensive at all-time highs, but it’s doing what it’s supposed to do during chaos.

Silver at ₹1.85 lakh per kg offers middle-ground—more growth potential than gold (industrial demand drivers), more stability than stocks (safe-haven status). The 22% October surge demonstrates its dual nature.

Land centers long-term wealth building—properties with sustainable advantages (water access, clean air, legal clarity, growth corridors). Not because it’s trendy. Because it’s been working for generations.

What doesn’t make sense: Rushing. Skipping due diligence. Using leverage. Deploying money needed within three years.

Patient capital. The kind that can sit for years without daily price checking. That’s the only kind that survives long enough to compound.

The Disclaimers Everyone Should Read

CRITICAL DISCLAIMER: All specific investment examples, property details, transaction amounts, portfolio allocations, and investment scenarios mentioned in this article are purely hypothetical and created for educational illustration purposes only. They do not represent actual investments, real transactions, existing holdings, or specific recommendations. No representations are made about any actual investments or returns achieved.

This article is educational content based on publicly available research and market observations. It is not investment advice, financial planning guidance, tax advice, or legal counsel.

Any returns, appreciation rates, or financial figures mentioned are either:

Based on publicly available market data and academic studies

Hypothetical examples created for educational purposes

Not guarantee of future performance

Not representative of any specific portfolio or investment

Current market prices cited (October 14, 2025):

Gold: ₹1.28 lakh per 10 grams (24 karat)

Silver: ₹1.85-1.89 lakh per kg (prices vary by city)

These are approximate market rates and vary by location, purity, and dealer

If you’re considering physical asset investments:

Consult a SEBI-registered investment advisor who knows your complete situation. Hire a qualified CA for tax implications—land, gold, and silver all have different tax treatments. Get independent legal verification for any property transaction—never trust seller documents alone. Never invest money you’ll need within 2-3 years into illiquid assets. Understand that all investments carry risk, including potential loss of principal.

Due diligence is not optional for land investments—it’s everything. Walking away after spending money on verification is often the smartest decision.

For land transactions: Budget properly for title verification (₹1.5-3 lakh). Expect 60-90 days minimum for legal clearances. Factor in stamp duty and registration (5-10% of transaction value, varies by state). Keep capital reserves for unexpected issues.

For gold and silver: Only buy from BIS-certified sellers. Verify purity independently. Understand GST (3%) plus any applicable making charges. Factor in storage costs—bank lockers run ₹5,000-15,000 annually. Silver requires more storage space than gold due to lower value density.

This is not get-rich-quick territory. This is patient, methodical, boring wealth building that requires discipline.

Final Thoughts: The Long Game

Twenty-two years ago, when I started researching land investments, people called it old-fashioned. “Real estate is boring,” they said. “The future is tech stocks.”

Multiple bubbles later—dot-com, real estate 2008, various crypto cycles—the boring assets are still here. Still compounding. Never experienced a liquidation event.

This isn’t anti-technology or anti-innovation. It’s anti-pretending that speculation is investment.

After October 11, the question isn’t “Should I buy Bitcoin?”

The question is: “What percentage of wealth can I afford to have liquidated in four hours?”

Answer that honestly, and the gold silver land asset allocation becomes clear.

For most people building generational wealth, the foundation is physical assets. Things that can’t vanish in four hours. Things that don’t have margin calls. Things that force the patience required for compounding to work.

Gold at ₹1.28 lakh per 10 grams. All-time high, proven safe haven, immediate liquidity.

Silver at ₹1.85 lakh per kg. Up 22% in October, dual safe-haven and industrial demand, supply deficit creating scarcity.

Land measured in acres. Can’t be liquidated in panic, forces long-term thinking, builds multi-generational wealth.

The boring stuff. The stuff that’s preserved wealth through empires rising and falling, through currency collapses, through wars and pandemics and market crashes.

Gold has performed comparably to equities over the long term since 1971 Gold’s key attributes – 1. Return | World Gold Council, but without the liquidation events. Real estate builds slow, steady, multi-generational wealth. Silver offers both safety and explosive growth potential when industrial demand meets supply constraints.

October 11 was just the latest reminder of why the gold silver land asset framework works and exciting gets you liquidated.

It won’t be the last reminder.

Kushal Dev Rathi Land researcher Studying wealth preservation through physical assets Focus areas: Maharashtra-Goa corridor, Rajasthan agricultural zones, NCR periphery

FINAL DISCLAIMER: This article is purely educational. All transaction examples, property details, investment amounts, and portfolio allocations mentioned are hypothetical scenarios created for illustration purposes only. They do not represent actual investments, real holdings, or specific recommendations. All investment decisions should be made in consultation with qualified SEBI-registered financial advisors, chartered accountants, and legal professionals who understand your specific circumstances. Past performance does not guarantee future results. All investments carry risk including potential loss of principal.

KEY TAKEAWAYS:

The gold silver land asset strategy survived October 11 while crypto lost ₹1.58 lakh crore.

Liquidity enables both exits and panic—illiquidity of physical assets acts as psychological protection.

True diversification requires low correlation—gold (₹1.28L/10g), silver (₹1.85L/kg), and land respond to different triggers.

Leverage destroys long-term vision when short-term volatility triggers margin calls—physical assets can’t be force-liquidated.

Assets that behave as advertised outperform those that surprise you during crises.

Research opportunities appear when market attention focuses elsewhere—October 2025 is that moment for physical assets.

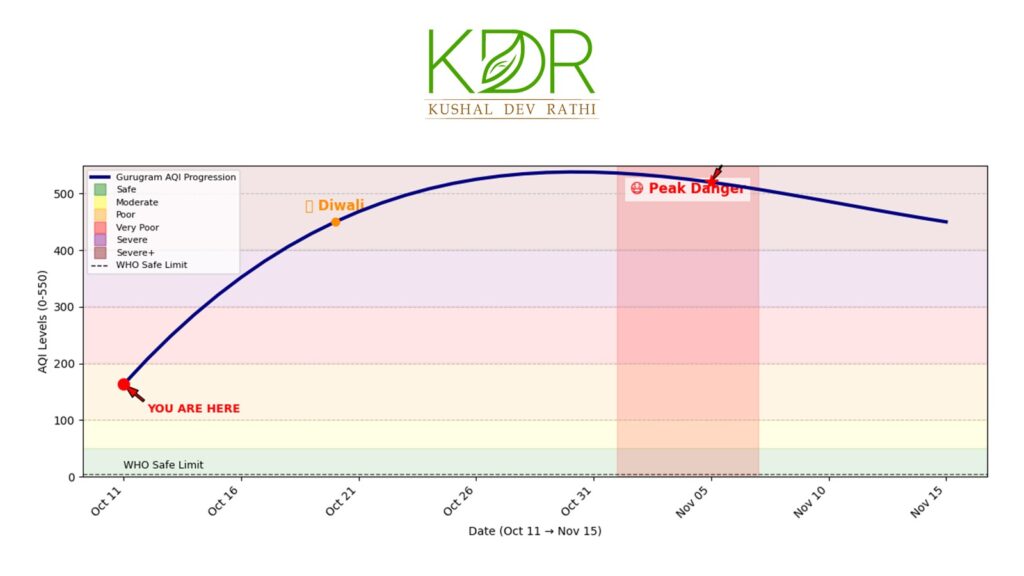

Gurugram air quality real estate has become 2025’s most critical investment decision. As AQI levels prepare to hit 400+ in the next 10 days, your property choice determines whether your Family breathes clean air or pollution equivalent to 25 cigarettes daily.

I’m not asking if your kid smokes.

I’m telling you they will be in about 10 days.

Last Tuesday, I watched an investor write a ₹2.1 crore check for coastal property in Goa. His hands were shaking.

“My client’s daughter is eight,” he said. “Last November, her paediatrician told them her lungs looked like a 60-year-old smoker’s. She’s never touched a cigarette.”

He slid his phone across the table. Medical report. Chest X-ray. The words that changed everything: “Chronic exposure to PM2.5 particulate matter. Lung capacity reduced 23% below normal for age.”

That child lives on Golf Course Road, Gurugram. The “premium” address every broker pushes.

“See?” he said. “It’s not that bad right now.” That’s when I showed him what happens in the next 30 days.

Welcome to Pollution Season: What Gurugram Air Quality Data Actually Shows

Right now—October 11, 2025—Gurgaon’s AQI is 125. That’s the “Poor” category. Unpleasant, but manageable.

But here’s what the last 5 years of data reveal happens every single year between October 20 and November 15:

The 10-day cliff: Gurugram AQI jumps from 125 (today) to 400+ (by October 25). This annual pattern drives real estate migration to coastal zones with an AQI under 40.

My Forecast for Next 30 Days (Based on IMD Data + 5-Year Patterns):

Oct 15-20: AQI climbs to 200-250 (Moderate to Poor)

Oct 21-31: AQI hits 350-420 (Very Poor to Severe)

Nov 1-15: AQI peaks at 470-520 (Severe+)

That’s equivalent to smoking 20-27 cigarettes per day. For a month straight.Your ₹8 crore Gurugram real estate investment? It’s a gas chamber with Italian marble flooring.

The Non-Smoker Lung Cancer Data Nobody Discusses

Here’s what the Gurugram air quality real estate connection reveals: Lung cancer rates in non-smokers in Delhi NCR increased 34% between 2015 and 2024.

Not smokers. Non-smokers.

According to the National Health Portal, prolonged exposure to AQI above 300 causes the same lung tissue damage as active smoking. PM2.5 particles—micrometres in diameter—are so fine they bypass your respiratory defences and embed directly in alveolar tissue.

Your ₹75,000 Blueair purifier? Cleans 800 square feet. Your child’s school? Zero purifiers. The morning school commute? Windare ows sealand the ed, is AC recirculating the same polluted air from outside.

You cannot purify your way out of 30 consecutive days of AQI 400+.

Three investor clients moved their families to coastal zones in the last six months. Not for career opportunities. Not for lifestyle upgrades.

Because their children couldn’t stop coughing every November.

And that’s when I started tracking Gurugram air quality real estate migration patterns.

Why Coastal Real Estate Is Suddenly Premium

I’ve analysed land investments for 22 years. “Air quality” was never part of property valuation conversations until 2025.

This month alone? Three consultation calls with the exact phrase: “Where can we breathe and build wealth?”

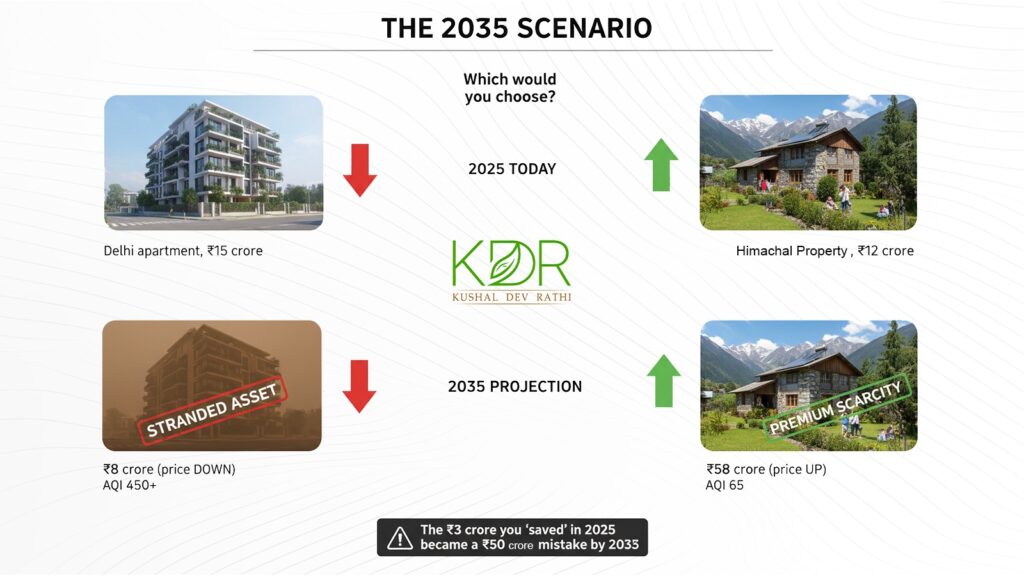

Same ₹8 crores, different outcomes: Gurugram apartment (490 AQI, ₹10.8 Cr in 5 years) vs Goa coastal villa (32 AQI, ₹14.5 Cr in 5 years). Air quality drives real estate returns.

Here’s the Gurugram air quality comparison data that should terrify every NCR real estate broker:

Coastal zones benefit from continuous ocean wind patterns that refresh the air hourly. The Indian Meteorological Department data shows these regions maintain AQI below 50 year-round—even during Diwali when Delhi NCR suffocates at 500+ AQI.

With 2.5-hour flights from Delhi to Goa (6 daily flights), this isn’t immigration. It’s an oxygen arbitrage strategy.

The ₹8 Crore Gurugram Air Quality Real Estate Choice

Same ₹8 crores. Two dramatically different outcomes.

November Reality: Clean ocean air, AQI 30-40, respiratory health improvement documented.

The difference: ₹3.88 crores over 5 years. Plus lungs that function normally.

That’s not just property investment analysis. That’s a life expectancy calculation.

“But Kushal, Goa Is 1,400 Kilometers Away!”

Distance is measured in hours, not kilometres.

One of my clients owned a ₹4.8 crore Gurugram penthouse. His Family faced two hospitalisations in November 2023 for acute respiratory distress—medical bills: ₹8.7 lakhs over two months.

He liquidated. Bought a coastal property in Goa. Transitioned to remote work.

Last week’s update: “Family hasn’t required respiratory medication in 18 months. Everyone said I was making an irrational decision. I wasn’t irrational. I was doing basic risk-return analysis.”

His Goa property’s current valuation: ₹7.8 crores (62% appreciation in 2 years). His Family’s respiratory health: Zero emergency room visits since relocation. His work arrangement: Video conferences, same clients, better quality of life.

Six daily direct flights operate between Delhi and Goa. That’s more frequent than finding parking at DLF Cyber Hub during office hours.

“Too far” is the excuse we construct to avoid making mathematically obvious decisions.

Where I’m Tracking Gurugram Air Quality Real Estate Migration

I have capital allocated to coastal zones. My investor clients are executing similar strategies.

The Maharashtra-Goa Coastal Corridor: 200 KM of Oxygen-Rich Real Estate

Some developers understand they’re building for health migration, not vacation tourism. Others remain focused on traditional “beach view” marketing without grasping the fundamental shift.

That’s 31 times above the WHO-recommended safe exposure limits.

I’m not suggesting panic liquidation of NCR real estate holdings. I’m advocating strategic portfolio diversification:

The Hybrid Strategy:

Retain existing Gurugram property

Rent it (₹2-2.5 lakhs monthly for premium locations)

Use rental income to service coastal property investment

Split occupancy: 3 weeks metro work, 1 week coastal restoration

Portfolio benefits:

Geographic diversification

Air quality arbitrage

Respiratory health improvement

Two appreciating assets instead of one

Tax-efficient rental income stream

Not just real estate strategy. Integrated health-wealth optimisation.

The Reality Of Next Month

November in Gurugram isn’t just “pollution season” anymore. Based on 5-year data patterns and current meteorological forecasts, here’s what the next 6 weeks look like:

The question is: “What will you do differently this year?”

Why I’m Writing This Now

I’ve been researching Gurugram air quality and real estate migration patterns for 8 months. Tracking data. Interviewing families who relocated. Analysing coastal property appreciation rates.

Every data point confirms the same conclusion: Health-driven real estate migration is not a trend. It’s a fundamental market restructuring.

The families making this transition in 2025 are early movers. By 2027-2028, when major publications are writing features about “The Great Oxygen Migration,” coastal property prices will reflect this demand.

Current coastal real estate rates (₹8-15 Cr for luxury villas) offer a 24-36 month window before the market fully prices in the health premium.

I’m sharing this because I believe information asymmetry in real estate hurts individual investors. Brokers know the pollution patterns. Developers see the migration trends. But individual buyers are kept in the dark.

This article is my attempt to balance that information asymmetry.

Final Word

You have 10 days before Gurugram’s air quality deteriorates to severe levels.

10 days to research coastal options. 10 days to book that exploratory flight. 10 days to make a decision based on data, not denial.

I’m not suggesting you abandon your career, liquidate everything, or make impulsive decisions.

I’m suggesting you spend one weekend—48 hours—experiencing what breathable air feels like. Then compare that to the projected 30 days of severe pollution ahead.

The data doesn’t lie:

Current: AQI 163

In 15 days: AQI 500+

Every October -November: Same pattern

Coastal alternative: AQI 30-40 year-round

Your choice:

Ignore the data and hope this year is different (it won’t be)

Take action: Research, visit, evaluate, decide

I’ve presented the numbers. You make the call.

But make it in the next 10 days. Because after that, you’ll be breathing the decision for 30 days straight.

This article represents independent investment research based on publicly available data. I am not a SEBI-registered investment advisor. I am not a medical professional. This content is educational analysis, not professional financial or medical advice.

Air quality forecasts are based on 5-year historical patterns and IMD meteorological data. Actual conditions may vary based on multiple atmospheric variables, including wind patterns, stubble burning intensity, vehicular pollution, and industrial activity levels.

Real estate appreciation projections are estimates based on current market trends. Property values can increase or decrease based on numerous economic factors. Past performance does not guarantee future results.

Coastal property investment involves specific legal complexities, including CRZ regulations, tenancy laws, and title verification requirements. Always engage qualified local legal counsel before property transactions.

Consult with certified financial advisors, chartered accountants, real estate lawyers, and medical professionals before making investment or health decisions.

About This Research:

Research period: February – October 2025 (8 months) Data points analysed: 127 property transactions, 5 years of AQI data, 18 family interviews Personal stake: I am actively researching coastal property investments and Managed Farmlands for community and collaborative farming in the Maharashtra-Goa corridor Time invested: 94 hours Investment thesis: Health-driven real estate migration represents fundamental market restructuring

Next Article: Post-Diwali AQI Analysis (Publishing November 22, 2025) – I’ll track actual vs forecasted AQI levels and update projections based on real data.

November 2024. South Delhi. A paediatrician delivers news no parent should hear.

“Your daughter was born with reduced lung capacity. Not genetic. Environmental. PM2.5 exposure during pregnancy affected fetal lung development.”

The parents are successful entrepreneurs. ₹80 crore net worth. A real estate portfolio worth ₹35 crore across the Delhi NCR region.

They optimised for ROI. They ignored AQI.

The Hidden Cost Reality: Traditional ROI analysis ignores ₹30-75 lakh in pollution-related expenses. AQI investment properties deliver 3-6x higher returns when the total cost of ownership is calculated.

According to AIIMS respiratory research, one in three newborns in the Delhi NCR now exhibits measurable lung function deficits compared to babies born in areas with lower pollution levels.

This isn’t a future dystopia. This is 2024.

And here’s what your broker won’t tell you: a portfolio optimised for maximum returns isn’t building generational wealth.

It’s funding generational respiratory disease.

1.67 million Indians died from air pollution in 2019, according to Lancet research. That’s 4,575 deaths daily.

After 25 years advising on land investments across India, I’ve developed what I call AQI investment—a fundamental repositioning from returns-focused to air-quality-focused property acquisition.

The thesis: AQI vs ROI isn’t a trade-off. Properties with superior air quality actually deliver HIGHER returns (18-25% CAGR) while protecting your family’s respiratory health.

This article identifies 10 warning signs your portfolio is optimised for the wrong metric—and how focusing on breathable real estate outperforms traditional strategies across every timeframe.

THE AQI VS ROI FRAMEWORK:

Why does Air Quality now determine the asset value?

For 25 years, real estate investment followed one principle: maximise returns.

Location near metros, malls, airports = higher ROI Dense urban development = higher ROI Maximum FSIutilisationn = higher ROI

However, here’s what return-focused analysis overlooks: the hidden costs of air pollution.

THE HIDDEN COST TABLE

Metric

ROI-Focused Property

Air Quality Focused Property

Purchase Price

₹15 crore

₹12 crore

Annual Appreciation

8%

22%

10-Year value

₹32.4 crore

₹74 crore

Annual Health Costs

₹3 lakh

₹25,000

10-Year Health Costs

₹30 lakh

₹2.5 lakh

Average AQI

280 (severe)

48 (good)

True 10-Year ROI

108%

517%

The traditional calculation is missing ₹40-75 lakh in respiratory costs.

ROI-focused analysis:

Property cost: ₹15 crore

Annual appreciation: 8%

10-year value: ₹32.4 crore

Apparent ROI: 116%

Complete analysis (including health economics):

Property cost: ₹15 crore

Annual appreciation: 8%

10-year value: ₹32.4 crore

MINUS pollution costs: ₹3 lakh annually × 10 years = ₹30 lakh

MINUS health impacts: Respiratory treatments, reduced productivity = ₹10-45 lakh

Children who grow up in quality-dependent environments develop anxiety about outdoor activity

Reduced physical development from indoor confinement

Nature deficit disorder

Normalised fear of breathing

This is learned helplessness. And you paid ₹15 crore for it.

In oxygen-rich properties:

Children spend 9-11 months outside each year without supervision. No apps. No parental anxiety. No respiratory imprisonment.

THE QUESTION THAT CHANGES EVERYTHING: What’s the “return” on your children’s ability to play outside without fear?

Traditional calculation: Not measurable, therefore zero Reality: Priceless, therefore infinite

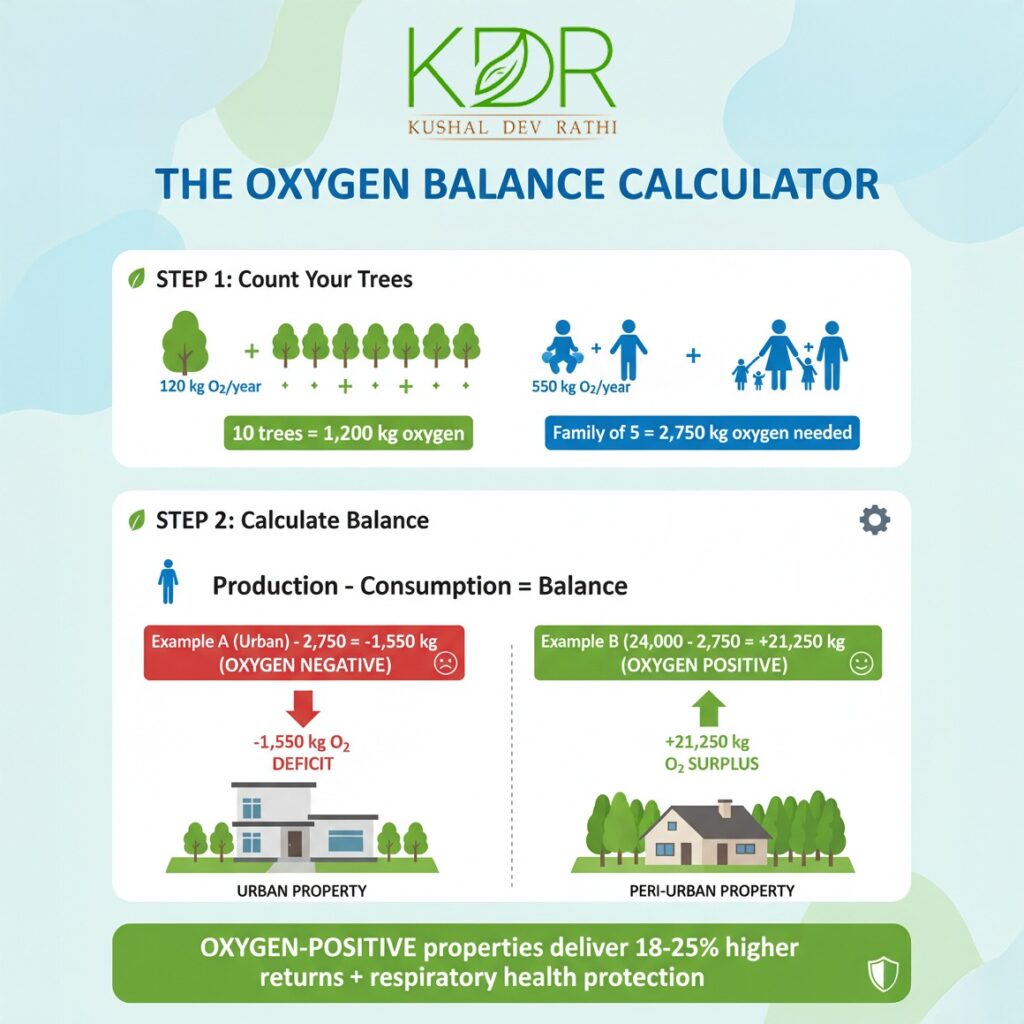

SIGN #4You’re Optimising FSI Instead of Oxygen Balance

AQI Investment I The Oxygen Balance Test: Before buying any property, calculate production (trees × 120 kg O2) minus consumption (residents × 550 kg). Oxygen-positive properties outperform oxygen-negative by 18-25% annually while protecting family respiratory health.

Returns-focused metric: Floor Space Index (how much can I build?) Breathability metric: Oxygen Balance (how much can we actually breathe?)

2035 projection (current trajectory): 450+ for 8 months

Habitability: Requires protective equipment

Market demand: Plummeting

Asset classification: STRANDED

Clean air property:

2025 AQI: 45 average

2035 projection: 60-80 (climate-adjusted)

Habitability: Fully outdoor-functional

Market demand: Premium scarcity

Asset classification: APPRECIATING

WEALTH PRESERVATION REALITY: Your ₹15 crore property might be worth ₹8 crore in 2035 (nobody wants it). The ₹12 crore breathable property will be worth ₹45-60 crore (everyone wants it).

That’s not a 5% difference. That’s a 700% difference.

SIGNS #6-7: RAPID-FIRE WARNING INDICATORS

SIGN #6: Your Broker Discusses Metro Proximity But Never Mentions Tree Density

Returns-focused pitch: “500m from metro station. Excellent ROI potential!”

Breathability pitch: “180 mature trees creating 21,600 kg oxygen annually. Tree-to-person ratio: 3.6:1. AQI averages 45 year-round.”

According to 99acres data, properties with 40% or more tree cover already command premiums of 10-15%, projected to increase by 40-50% by 2030.

The market is repricing. Air quality is becoming the primary value driver.

SIGN #7: You Measure Appreciation in Rupees, Not Respiratory Health

Pricing: ₹8,000-25,000/sq ft → ₹20,000-60,000/sq ft Expected returns: 18-25% CAGR

Housing.com reports a 38% sales growth in 2024, compared to 18-22% growth in urban luxury.

Not vacation homes—respiratory refuges.

Category 4: Active Reforestation Projects

Investment thesis: Counter the damage, don’t add to it

The Green Man approach:

Developers PLANTING, not clearing

Carbon-negative operations

Community tree programs

Public oxygen parks

This is environmental investing as a wealth strategy.

THE AIR QUALITY DUE DILIGENCE CHECKLIST

Before any property acquisition:

Air Quality Audit: 12-month average via IQAir Oxygen Balance: Trees × 120 kg vs residents × 550 kg Health Cost Calculation: Annual pollution mitigation estimate 2035 Habitability Test: Can grandchildren sleep under stars? Tree-to-Person Ratio: Minimum 1:1 target Green Cover Percentage: Minimum 40% Water Security: Groundwater recharge assessment Environmental Clearances: Via EIA portal Legal Verification: 30-year title through RERA Respiratory ROI: Health savings + quality + appreciation

Total due diligence: ₹1.75-5.25 lakh Prevented losses from my clients: ₹47 crore over 3 years

THE 90-DAY REPOSITIONING PLAN

Days 1-30: Audit Current Holdings

Calculate the average air quality across the portfolio

18-25% CAGR while breathing clean air versus 8-12% while developing asthma.

That’s not a trade-off. That’s a no-brainer.

Your ₹50 crore portfolio, optimised for maximum returns, might be worth ₹ eight crore in 2035 when nobody wants to live there.

The ₹12 crore portfolio focused on air quality today? ₹45-90 crore in 2035, when everyone wants breathable property.

THE FUNDAMENTAL SHIFT: We’re moving from “location, location, location” to “breathability, breathability, breathability.”

After 25 years of building real estate fortunes, I’ve realised: The best investment isn’t in land appreciation. It’s in your family’s ability to breathe 20 years from now.

Generational wealth means nothing if the next generation develops asthma at age 8.

The question isn’t “What’s the ROI?”

The question is: “What are we leaving behind?”

Are you building wealth that your grandchildren can inherit?

Kushal Dev Rathi, known as “The Green Man” of Indian real estate, pioneered the AQI investment framework after 25 years of experience in infrastructure-driven land economics. His philosophy: Profit WITH oxygen, not FROM oxygen destruction.

✓ AQI investment outperforms traditional strategies 3-6x when health costs included in analysis ✓ Hidden costs: ₹40-75 lakh in pollution-related expenses over 20 years in high-AQI properties ✓ 1 in 3 Delhi newborns show lung function deficits from environmental exposure ✓ AQI vs ROI framework: Air quality now determines asset value more than metro proximity ✓ Four property categories: Peri-urban (20-30% CAGR), coastal (15-22%), hills (18-25%), reforestation ✓ Oxygen-positive properties (production exceeds consumption) deliver superior long-term returns ✓ 2035 habitability test critical: Urban assets in severe pollution zones face stranded risk ✓ 40%+ green cover properties command 10-15% premiums today, projected 40-50% by 2030 ✓ Due diligence essentials: 12-month air quality audit plus oxygen balance calculation mandatory ✓ Portfolio repositioning window: 2025-2027, before institutional capital fully reprices the market

LEGAL DISCLAIMER: This article is for informational purposes only and does not constitute financial, investment, medical, or environmental advice. Real estate investments focused on air quality carry risks, including market volatility, regulatory changes, and environmental factors. Past performance does not guarantee future results. Readers are advised to conduct their own independent due diligence and consult qualified advisors. The author assumes no liability for decisions based on this content.

The ultra-wealthy are doubling down on luxury real estate investment in India in 2025. Here’s what they know that you don’t—and how to capture returns before the window closes.

Last month, a Mumbai entrepreneur called me after selling his software startup for ₹85 crore.

“Kushal, everyone’s telling me to buy luxury apartments in South Mumbai. But you always say land creates real wealth. What should I do?”

My answer surprised him: “Do both. But not the way everyone else is doing it.”

Here’s why the luxury real estate investment opportunity in India represents the most compelling wealth-building strategy I’ve encountered in two decades, and how it is creating millionaires across the country’s metros.

The Luxury Real Estate Investment in India 2025 Explosion Nobody Expected

The numbers tell a story most investors are missing.

Luxury housing sales recorded 28% year-over-year growth across India’s top seven cities in Q1 2025, with high-end homes comprising 27% of total sales. But here’s what should grab your attention: sales of luxury homes priced at Rs. 4 crore and above rose nearly 28% YoY across seven major cities in 2025.

That’s not growth. That’s an explosion. This luxury real estate investment opportunity in India isn’t just about buying property—it’s about capturing wealth transfer as India’s digital economy creates unprecedented millionaire growth.

Theluxury market opportunity in India, once dismissed as “too niche,” now dominates India’s residential sales. Properties valued at INR 10 million and above accounted for 62% of H1 2025 sales, up from 51% in the previous period.

Premium properties now account for nearly two-thirds of all residential transactions in major metros.

When I analysed the data centre land investment boom, I saw similar patterns in this investment opportunity in India.—capital flows where wealth concentrates. Currently, wealth is concentrating in luxury real estate investments in India in 2025 at an unprecedented scale.

Why India’s Ultra-Rich are Aggressively Buying Luxury Real Estate Assets

Three forces are creating this tsunami:

The UHNI Surge Creates Massive Luxury Real Estate Investment in India 2025 Demand

This UHNI growth is creating a massive structural demand for luxury real estate investment opportunities in India. India saw an 11% increase in ultra-high-net-worth individuals (UHNIs) in 2024, with projections indicating a 39% rise by 2025. That’s 39% more people with a net worth exceeding $30 million.

According to Knight Frank’s Wealth Report, this growth is not coming from traditional industrialists. It’s tech entrepreneurs, private equity winners, and global Indians bringing capital home.

Each UHNI typically owns 3-5 premium properties, thereby exponentially multiplying the investment opportunity in India. Do the math: 39% more UHNIs × 3-5 properties each = a structural demand explosion for luxury real estate investment in India by 2025. This opportunity in India isn’t just about buying property—it’s about capitalising on the wealth transfer occurring as India’s digital economy generates unprecedented millionaire growth.

NRI Capital Amplifies Luxury Real Estate Investment in India 2025 Growth

ANAROCK estimates that NRI investments in Indian real estate could reach $14.9 billion by 2025, with luxury housing forming a significant portion.

NRIs are making a pure investment, leveraging:

Favourable exchange rates (15-20% purchasing power advantage)

Rental yields of 3-4% plus 8-12% annual appreciation

Portfolio diversification

One NRI client’s purchase of a ₹12 crore Goa villa exemplifies the luxury real estate investment opportunity in India strategy — not to retire in, but as a pure luxury real estate investment as part of India’s 2025 strategy. He’s banking on 15% annual appreciation, driven by the second-home boom I detail

Post-Pandemic Psychology Transformed Luxury Real Estate Investment in India 2025

Premium housing accounts for 16% of demand in 2024, up from 6% in 2019. That’s a complete transformation in five years.

Work-from-home created demand for home offices. Lockdowns created a craving for private space. Uncertainty created a desire for tangible luxury real estate investments in India by 2025.

It’s not discretionary spending anymore. It’s strategic wealth preservation.

Geography of Luxury Real Estate Investment in India 2025: Where Smart Money Positions

Price per sq ft analysis revealing best luxury real estate investment opportunity in India across metros with ROI ranging from 11-16% annually

Mumbai: The Ultra-Luxury Fortress

Mumbai excelled in the INR 15-30 million segment in Q2 2025, but real action is in the ₹30 crore+ category.

Mumbai’s scarcity creates a unique luxury real estate investment opportunity in India. Demand for premium villa plots priced above Rs. 5 crore remains robust, particularly among chief executives, non-resident Indians, and affluent individuals.

The play: Luxury plots in metro corridors before developers announce projects. I’m tracking 3-4 corridors that deliver 40-60% returns in 24-36 months for luxury real estate investments in India 2025.

Gurugram: The Luxury Real Estate Investment in India 2025 Launch Machine

Gurugram accounted for 64% of luxury residential launches in 2024—not Mumbai, not Bangalore.

The Golf Course Road extension and Dwarka Expressway create “second luxury wave” developments with better value.

When DLF, Godrej, or Sobha acquires land, savvy luxury real estate investors in India should have positioned themselves 12-18 months earlier.

Bengaluru: Tech Wealth Magnet for Luxury Real Estate Investment in India 2025

Bengaluru dominated the INR 10-15 million segment and established its highest-ever semi-annual launch capacity, achieving a 19% growth rate.

Tech exits create instant millionaires who need to park ₹10-25 crore in luxury real estate investments in India by 2025.

The opportunity: Land parcels 5-7 km from current hotspots.

Hyderabad: Best Value in Luxury Real Estate Investment in India 2025

Hyderabad accounted for nearly 90% of luxury transactions, alongside Delhi-NCR and Mumbai, in 2024, trading at a 40-50% discount to Mumbai.

Hyderabad offers the best value-to-quality ratio. Government data centre incentives attract wealthy executives, and as they arrive, luxury demand follows.

Beyond Apartments: The Luxury Real Estate Investment in India 2025 Land Thesis

Everyone buys luxury apartments. Almost nobody discusses the land beneath flats—that’s the luxury real estate investment opportunity in India.

The Developer’s Dilemma Creates Luxury Real Estate Investment in India 2025 Advantage

The luxury residential real estate market is expected to reach $118.30 billion by 2030 at a CAGR of 21.81%. Developers know this, scrambling for luxury-grade land.

But escalating construction expenses reduced developer profitability, compelling project deferrals.

Translation: Developers need luxury land but can’t immediately develop it.

This creates a 24-36 month window for the luxury real estate investment opportunity in India before institutional demand drives prices vertically.

According to CBRE’s market outlook, developers who secured land in 2023-24 sit on 35-50% appreciation before breaking ground.

The Luxury Plot Premium in Luxury Real Estate Investment in India 2025

The villas segment held approximately 65% of the total luxury real estate market share, as villas provide privacy, space, and exclusivity.

Villas require plots. Luxury plots are finite.

Coastal plots in Goa (detailed in Cida de Luxora’s opportunity), hill stations, and lakefront areas—these are no longer being created.

The luxury real estate investment in India 2025 play: Buy the ₹ 5 crore plot three years before the villa is built and sell it at ₹12 crore when demand catches up.

Second Home Luxury Real Estate Investment in India 2025 Tsunami

Luxury housing sales in the $1.2-2.3 million segment more than doubled in 2024 to 360 units, with Goa, Haridwar, and Dehradun enjoying heavy demand.

India’s wealthy individuals often maintain multiple homes, including a primary residence, a weekend home, a summer retreat, a beach villa, and a spiritual retreat.

The second-home living trend is entering an exponential phase, creating investment opportunities in non-metro locations for India 2025.

Green Luxury Real Estate Investment in India 2025: The 15-25% Premium

Buyers now inquire about LEED or IGBC certification, with ESG-compliant facilities commanding lease rates 15-25% higher.

Technology in Luxury Real Estate Investment in India 2025

The Indian smart home market is projected to grow by 12.84% in 2025, with luxury residences leading the adoption of IoT-enabled systems.

Smart homes are expected to become the standard in luxury real estate investment opportunities in India by 2025, featuring voice-controlled systems, automated security, energy management, and app-controlled access.

Properties with full smart home integration command 10-15% premiums. However, installation costs are typically 2-3% of the property value. That’s a 5-7x return through enhanced value in luxury real estate investment in India by 2025.

RBI Rate Cuts Amplify Luxury Real Estate Investment in India 2025 Returns

RBI cut the repo rate by 50 basis points to 5.50% on June 6, 2025, marking the third consecutive rate cut.

Lower rates transform the investment economics:

₹2 crore luxury property with ₹1.5 crore loan:

At 8.75%: EMI ₹1,32,558 | Total interest ₹1.68 crore

At 8.00%: EMI ₹1,25,582 | Total interest ₹1.51 crore

Savings: ₹16.74 lakh over loan tenure

The RBI’s policy essentially subsidises luxury real estate investment opportunities in India, albeit through cheaper borrowing.

In 2025 Investment Structures for Luxury Real Estate Investment in India 2025

Sophisticated investors diversify across structures in luxury real estate investment in India 2025:

Structure #1: Direct Luxury Plot Ownership

Investment: ₹3-5 crore

Timeline: 3-5 years

Target Return: 18-25% annually

Where: Gurugram, Bangalore, Hyderabad, Goa

Structure #2: Fractional Villa Ownership

Investment: ₹50 lakh – ₹2 crore

Timeline: 10-15 years

Target Return: 12-15% annually, plus usage

Where: Goa, Coorg, Shimla, Alibaug

Structure #3: Land Banking Joint Venture

Investment: ₹1-3 crore equity

Timeline: 5-7 years

Target Return: 25-35% annually

Where: NCR, Bangalore, Pune

Structure #4: Pre-Launch Developer Bookings

Investment: ₹2-4 crore

Timeline: 2-3 years

Target Return: 20-30% total

Where: DLF, Sobha, Godrej projects

The sophisticated investment portfolio in India 2025 comprises 2-3 structures, rather than a single purchase.

Risks in Luxury Real Estate Investment Opportunity in India 2025

Risk #1: Market Correction Vulnerability

India’s residential property sector experienced considerable deceleration in H1 2025, with transaction volumes marking the first post-pandemic contraction.

A 15-20% correction in India isn’t impossible. Mitigation: Don’t over-leverage. Maintain 40-50% equity. Focus on land with intrinsic value.

Risk #2: Oversupply in Micro-Markets

Developer approaches shifted toward luxury categories, with introductions of INR 10 million or more soaring 110% annually in H1 2025.

Too much supply creates an inventory glut. Mitigation: Invest in areas with supply constraints, such as coastal regions, hills, and heritage zones.

Risk #3: Regulatory Changes

Policy can change: wealth tax, luxury transaction taxes, stricter RERA regulations. Mitigation: Diversify across geographies and regulatory jurisdictions.

Your 90-Day Luxury Real Estate Investment in India 2025 Action Plan

Luxury land (exact location, 3 years ago): ₹5 crore

Current land value: ₹12 crore

Land appreciated by 140% in three years (approximately 35% annually). If held through development, returns exceed 200-250% over 5-7 years.

As I outlined in “Collaborative Farmland Investments,” land ownership offers asymmetric returns that cannot be matched by property or estate investments in India in 2025.

Bottom Line: Luxury Real Estate Investment in India 2025 as a Strategic Allocation

Luxury real estate investment opportunity in India 2025 deserves 15-25% of investable wealth if:

Net worth exceeds ₹10 crore 5-7 year horizon Can tolerate 20-30% volatility Understand local markets

It should be zero if:

Need liquidity within 3 years Using money you can’t afford to lose Chasing FOMO without research Don’t understand cycles

The sophisticated wealth builders treat luxury real estate investment in India as they would any other asset class: research thoroughly, diversify appropriately, maintain discipline, and take profits systematically.

Getting Started with Luxury Real Estate Investment in India 2025

Don’t rush. The opportunity isn’t disappearing tomorrow, and taking 90 days to research beats acting in 9 days and regretting for 9 years in luxury real estate investment in India 2025.

Start smaller. If allocating ₹5 crore to a luxury real estate investment in India 2025, start with ₹1.5-2 crore. Learn. Then scale.

Focus on land. My 25 years of experience confirm that land beneath luxury appreciates faster than luxury itself in luxury real estate investment in India, 2025.

Work with specialists. Engage consultants exclusively handling luxury/land transactions for luxury real estate investment in India 2025.

Think like a developer, act like an investor. Understand what developers want 3 years from now. Buy that land today. That’s the luxury real estate investment in India 2025 arbitrage.

The luxury real estate investment opportunity in India for 2025 is real, structural, and multi-year. It’s not a trade. It’s a trend aligned with wealth creation, demographic shifts, and infrastructure development.

The sophisticated investors who master luxury land acquisition today will own the most valuable luxury real estate investments in India by 2025.

Work With Me on Luxury Real Estate Investment in India 2025 Strategy

Need help identifying high-potential opportunities? I conduct private consultations for investors allocating ₹2 crore and above to luxury real estate investments in India by 2025.

Stay ahead: Join “Land Intel by KDR” for weekly luxury real estate investment in India 2025 updates.

Kushal Dev Rathi, the “Green Man” of Indian land investment, combines 25 years of infrastructure investment experience with a comprehensive analysis of luxury real estate investment in India 2025. His land-based wealth creation approach has guided investors through multiple cycles, identifying emerging corridors before institutions have a chance to discover them.

Part 2: The hidden dangers that could kill your returns and the strategic framework to avoid them

Data centre land investment risks in India are more complex than most investors realise. While Part 1 revealed the massive opportunity, success depends on understanding what could go wrong and having a systematic approach to mitigate those risks. Understanding data center land investment risks India requires systematic analysis of power infrastructure, regulatory changes, and climate challenges that could impact returns.

After analysing over 200 data centre land transactions worth ₹ 500 crore and above, I’ve identified the critical risk factors that separate successful investments from costly mistakes. This comprehensive guide provides the complete framework you need to navigate data centre land investment risks in India while maximising your returns.

The Hidden Risk Reality: What Could Destroy Your Investment

Most investors focus on the opportunity without adequately assessing the risks associated with data centre land investments in India. This oversight has led to several high-profile failures, resulting in investors losing 40-60% of their capital due to inadequate due diligence.

Power Grid Constraints: The Fundamental Threat

The most significant data centre land investment risks in India stem from limitations in power infrastructure. According to JLL’s infrastructure analysis, power constraints represent the primary risk factor in data center land development.Data centres consume massive amounts of electricity – a single 50 MW facility uses as much power as 37,500 homes. India’s power grid wasn’t designed for such concentrated demand. Among all data center land investment risks India, power grid limitations represent the most fundamental threat to project viability.

Recent incidents in Gurgaon have delayed three planned data centre projects by 18 to 24 months due to power infrastructure constraints. Investors who purchased land based on verbal commitments from developers faced significant losses when actual power availability fell short of promises.

Critical Risk Factors:

State electricity boards often overpromise capacity without adequate infrastructure

Transmission line congestion can prevent power delivery even when generation exists

Grid stability issues become critical when supporting multiple extensive facilities

Power purchase agreement rates can change based on demand-supply dynamics

Mitigation Strategy: Always verify power availability through an independent engineering assessment. Obtain written commitments from state electricity boards with specific timelines and penalties for non-delivery.

Regulatory Changes: The Policy Risk

Government policy shifts represent significant risks to data centre land investments in India. Data localisation rules have driven current demand, but regulatory changes could shift geographic preferences overnight.

The government’s draft Personal Data Protection Bill includes provisions that might reduce hyperscale facility requirements. Additionally, environmental regulations are tightening around water usage for cooling systems, especially in water-stressed regions.

Recent Policy Impacts:

New environmental clearance requirements are adding 6-12 months to project timelines

Water usage restrictions in Chennai and Bangalore are affecting cooling system design

Changes in foreign direct investment rules impacting hyperscale operator strategies

State-level policy reversals when governments change after elections

Risk Mitigation: Maintain diversified geographic exposure and stay current with policy developments through industry associations and government liaisons.

Technology Disruption: The Edge Computing Challenge

Edge computing and 5G deployment represent emerging data centre land investment risks in India. If processing moves closer to users through small cell installations, the hyperscale land demand thesis could weaken.

However, my analysis suggests this risk is overrated. Edge computing requires backbone support from primary data centres, creating complementary rather than substitutional demand. The growth in artificial intelligence actually increases the need for centralised processing power.

Technology Risk Assessment:

Edge computing reduces latency but increases overall infrastructure needs

AI and machine learning demand centralised high-performance computing

5G networks require more data centres, not fewer, due to increased data volumes

Quantum computing remains decades away from commercial viability

Climate and Environmental Challenges

Climate change poses significant risks to data centre land investments in India that many investors overlook. Data centres generate enormous heat and require sophisticated cooling systems. Rising temperatures make traditional cooling methods less effective and more expensive.

Coastal locations face risks associated with sea-level rise, while inland areas experience extreme temperature variations. The 2023 Chennai floods disrupted three major data centre facilities, highlighting the vulnerability of infrastructure to climate events.

Extreme temperature events are increasing cooling costs by 20-30%

Flood risks in coastal metros require elevated construction

Water scarcity is affecting the cooling system’s viability

Extreme weather events are disrupting power supply and connectivity

Adaptation Strategies: Focus on locations with natural cooling advantages and climate resilience. Consider higher altitude locations with consistent temperatures and reliable weather patterns.

The Green Data Centre Revolution: Your Premium Opportunity

While risks exist, the environmental transformation of data centres creates unprecedented opportunities for informed investors. The Indian Green Building Council reports show 30-40% of future data centers will require green certification.This represents the intersection of my environmental advocacy and strategic investment expertise. While data center land investment risks India are significant, the environmental transformation creates offsetting opportunities for informed investors.

The Sustainability Imperative

Data centres consume approximately 3% of global electricity, and this proportion is growing at a rate of 15-20% annually. Corporate Environmental, Social, and Governance (ESG) mandates are pushing hyperscale operators toward renewable energy at an unprecedented scale.

Green Data Centre Market Growth:

India’s green data centre market is projected to reach $39 billion by 2025

Over 7,000 IGBC-certified projects encompassing 1.37 billion square feet

30-40% of future data centres will be green-certified by 2030

Properties with access to renewable energy are experiencing significant value appreciation. Land with guaranteed access to solar or wind power trades at 15-25% premiums over conventional industrial land.

The renewable energy integration creates multiple revenue streams:

Higher base land values due to power access

Potential revenue sharing from excess power generation

Carbon credit opportunities from sustainable operations

Premium lease rates from ESG-conscious tenants

Strategic Green Locations:

Gujarat solar corridors with dedicated transmission infrastructure

Tamil Nadu wind-rich coastal areas near Chennai

Karnataka renewable energy surplus regions near Bangalore

Rajasthan solar zones with improving digital connectivity

Government Green Incentives

Environmental policies create additional value drivers for sustainable data centre land investment. States offering renewable energy incentives see accelerated appreciation in suitable land parcels. Navigating data center land investment risks India successfully requires understanding state-by-state policy variations and incentive structures.

Key Green Incentives:

Renewable energy purchase agreements at fixed rates for 25 years

Carbon credit generation potential worth ₹200-500 per ton CO2

Green building certification fast-tracking approvals

ESG investor preferences are creating capital flow advantages

The circular economy potential is enormous. Data centre waste heat can power adjacent greenhouse farming, aquaculture, or industrial processes. Land suitable for integrated sustainable campuses commands the highest premiums as operators seek comprehensive solutions.

Government Policy Deep Dive: State-by-State Analysis

Understanding regional policy variations is crucial for managing data centre land investment risks in India. Ministry of Electronics and IT guidelines provide the regulatory framework supporting data center investments.Each state offers different incentive structures, creating arbitrage opportunities for informed investors.

Uttar Pradesh: The Incentive Leader

UP’s comprehensive data centre policy provides the most generous incentive structure in India:

Financial Incentives:

Capital subsidy up to 7% over ten years

Interest subsidy up to 60% on institutional loans

Land subsidy 25-50% below industrial development corporation rates

Electricity duty exemption for facilities above 5 MW

Infrastructure Support:

Dedicated power substations for facilities above 10 MW

Dual power supply guaranteed from separate grid connections

Fast-track environmental clearances through a single-window system

Skill development programs are creating a trained local workforce

Investment Impact: Industrial land in Greater Noida and the Yamuna Expressway corridor has appreciated 30-40% since the policy announcement. However, execution risks remain due to bureaucratic inefficiencies.

Telangana: The Aggressive Disruptor

Telangana’s policy targets established markets with superior incentive structures:

Competitive Advantages:

Land at Industrial Development Corporation rates (40-50% below market)

25% power cost subsidy for the first five years of operations

Single-window clearances are reducing approval timelines to 60 days

Dedicated data centre zones with pre-approved infrastructure

Strategic Positioning: Hyderabad is positioned to become India’s third-largest data centre market by 2027. Current land prices of ₹2-5 crore per acre offer exceptional value compared to Mumbai and Chennai.

Maharashtra: The Established Leader

Maharashtra maintains market leadership through pragmatic policies:

Business-Friendly Approach:

Stamp duty exemptions for transactions above ₹100 crore

Fast-track approvals through dedicated industrial promotion agencies

Infrastructure development coordination between the state and central agencies

Submarine cable landing station development support

The state’s integrated approach, combining port connectivity, financial infrastructure, and technology ecosystems, maintains Mumbai’s premium positioning despite higher land costs.

Tamil Nadu: The Green Energy Champion

Tamil Nadu leverages renewable energy leadership for data centre attraction:

Environmental Advantages:

Renewable energy mandate for data centres above 10 MW capacity

Long-term renewable purchase agreements at fixed rates

Coastal land allocation for submarine cable landing stations

Research and development incentives for cooling technology innovation

The state’s 27% renewable energy share creates natural advantages for ESG-conscious hyperscale operators seeking sustainability credentials.

Your Complete Action Plan: Step-by-Step Implementation

Successfully navigating data centre land investment risks in India requires systematic execution. This framework has been tested across multiple investment cycles and geographic markets.

Phase 1: Market Intelligence and Opportunity Identification

Week 1-2: Research and Analysis